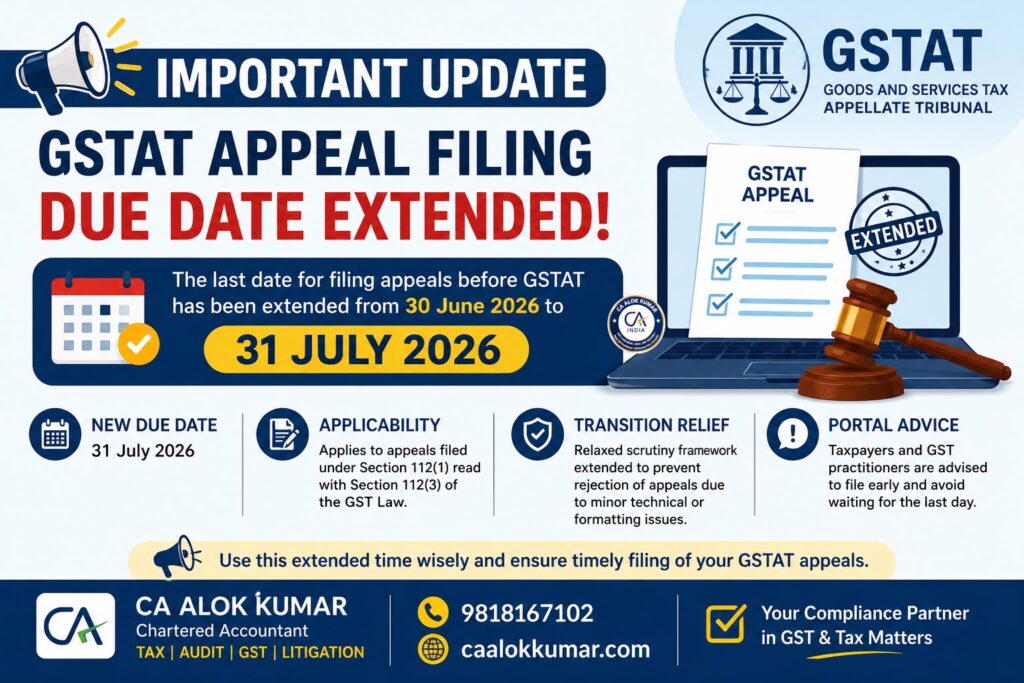

Filing GSTAT Appeal Due Date Extended to 31 July 2026: Important Update for Taxpayers

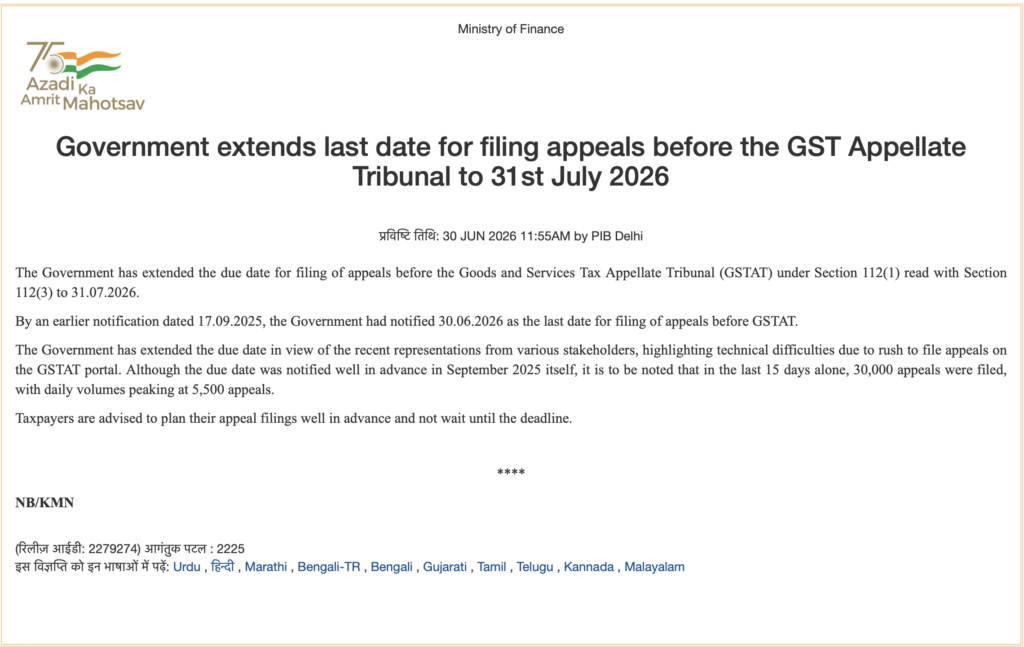

The Government has extended the due date for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) to 31 July 2026. This extension applies to appeals under Section 112(1) read with Section 112(3) of the CGST Act, 2017. Earlier, the last date notified for filing GSTAT appeals was 30 June 2026. (Press Information Bureau)

The extension has been granted because several taxpayers and professionals faced technical difficulties on the GSTAT portal due to heavy rush in filing appeals. As per the Ministry of Finance, nearly 30,000 appeals were filed in the last 15 days, with daily filing volume reaching around 5,500 appeals. The Government has also advised taxpayers not to wait until the last date and to complete filing well in advance. (Press Information Bureau)

Why This GSTAT Extension Matters

GSTAT is the second appellate forum under GST law. A taxpayer generally approaches GSTAT after receiving an adverse order from the First Appellate Authority under Section 107 or from the Revisional Authority under Section 108. The GSTAT portal also confirms that the last date for filing appeals under Section 112 of the CGST Act has been extended till 31 July 2026. (GSTAT)

Taxpayers having pending second appeal matters should immediately review their order, limitation period, disputed demand, pre-deposit requirement and supporting documents for timely GSTAT appeal filing.

Applicability of the Extended Due Date

As per the updated notification text, appeals relating to orders communicated before 1 May 2026 may be filed up to 31 July 2026. For orders communicated on or after 1 May 2026, the normal time limit of three months from the date of communication under Section 112(1) will apply. Similarly, departmental applications relating to orders passed before 1 February 2026 may be filed up to 31 July 2026, while later cases will follow the normal six-month period under Section 112(3).

Therefore, taxpayers should not assume that every GST matter automatically gets time up to 31 July 2026. The date of communication of the appellate or revisional order must be checked carefully.

Documents and Preparation Required

A GSTAT appeal is not only a portal filing exercise. It requires proper drafting and compilation of:

- Order-in-Original and Order-in-Appeal

- Show Cause Notice and demand summary

- Statement of facts

- Grounds of appeal

- Pre-deposit calculation

- Proof of payment

- Authorisation / Vakalatnama

- Supporting reconciliations and legal submissions

Professional support is important because incorrect drafting, incomplete documents or wrong computation of pre-deposit may weaken the appeal at the first stage itself.

Professional Assistance for GST Appeals and Demands

For taxpayers who have received an adverse first appellate order, our office provides end-to-end GSTAT appeal filing support, including appeal drafting, Form APL-05 e-filing, pre-deposit computation, document compilation, stay of demand and hearing representation before GSTAT. The service page also covers GSTAT representation, interlocutory applications, cross-objections and pre-deposit support. (CA Alok Kumar)

Where the matter is still at the first appeal stage, taxpayers may require GST appeal filing in APL-01 under Section 107. This includes order analysis, merit assessment, drafting of grounds of appeal, statement of facts, 10% pre-deposit computation, GST portal filing and representation before the Appellate Authority. (CA Alok Kumar)

Where the matter is at notice, SCN, DRC-01, ASMT-10 or DRC-07 stage, taxpayers should first prepare a proper GST notice and demand defence. This includes reconciliation, reply drafting, legal submissions, personal hearing representation, rectification advice, appeal viability review and recovery protection strategy. (CA Alok Kumar)

Key Takeaway

The GSTAT appeal filing due date extension to 31 July 2026 is a major relief, but taxpayers should not delay filing. GST disputes should be reviewed immediately, documents should be compiled, pre-deposit should be calculated correctly and appeal grounds should be professionally drafted. Early filing will help avoid last-minute portal issues, limitation risks and recovery complications.

For assistance in GSTAT appeals, first appeals, GST notices or demand defence, taxpayers may consult CA Alok Kumar, Chartered Accountant, for professional GST litigation and appellate support.

Leave a Reply