A landmark ruling by the Delhi High Court nullified the Commissioner of Delhi Goods and Service Tax’s order to cancel a physical verification for a GST registration that was conducted without the assessee’s authorised agent present.

Brief History of the Case :-

The government performed an inspection of the petitioner’s property before issuing a show-cause notice for registration revocation. The cancellation order was subsequently passed. The petitioner filed the writ petition in an effort to overturn the show cause notice (SCN) and subsequent order cancelling registration because they were based on a letter that the petitioner was not sent.

It was argued that if the relevant officer chose to conduct a physical inspection of the petitioner’s business premises, the inspection could only be conducted in the presence of the petitioner’s authorised representative in accordance with Rule 25 of the CGST Rules, 2017.

A landmark ruling by the Delhi High Court nullified the Commissioner of Delhi Goods and Service Tax’s order to cancel a physical verification for a GST registration that was conducted without the assessee’s authorised agent present. In a Coram, Mr. Justice Rajiv Shakdher and Ms. Justice Tara Vitasta Ganju noted that the application of the trader must be properly considered in the matter of registration under the GST Acts, and appropriate opportunity must be given to the applicant in the event of any unfavourable approach by the authorities. The petitioner, M/s Curil Tradex Pvt. Ltd., had its registration suspended by the respondents/revenue as of the day the show-cause notice was issued.

The relevant part of the aforementioned show cause notice is extracted hereafter:

“Whereas on the basis of information which has come to my notice, it appears that your registration is liable to be cancelled for the following reasons:

1. Letter dt. 6.04.2022 received DC, CGST-Delhi South Commissionerate – the firm is non existent. You are hereby directed to furnish a reply to the notice within seven working days from the date of service of this notice. If you fail to furnish a reply within the stipulated date or fail to appear for personal hearing on the appointed date and time, the case will be decided ex-parte on the basis of available records and on merits. Please note that your registration stands suspended with effect from 12/04/2022.”

The inspection was conducted on April 13, 2022, without the petitioner’s authorised representative present, according to Mr. Sameer Vashisht, who is in attendance on behalf of the respondents/revenue. He also claims that the verification report was uploaded on April 18, 2022. The petitioner deals with scrap material, thus there is a steady flow of material delivered into the business premises, according to Mrs. Manish. She also maintained that the images attached by the respondents/revenue do not prove that the petitioner does not do business at the subject premises. It was also asserted that since the petitioner’s authorised representative was required to remain on the property, he or she might have provided an explanation of the facts discovered there. According to the Court, “the proper officer could only physically inspect the petitioner’s company premises in the presence of its authorised representative.” In other words, the appropriate officer would need to serve a previous notice or notification in such a case. The writ petition was dismissed by allowing the petitioner to submit an application for the revocation of the cancellation order within the following 15 days and ruling that “once an application is filed, the same will be adjudicated by the concerned officer within two weeks of the date of submission of the application.”

Honourable High Court Order

The Honorable High Court said that it was undisputable in the current instance that the department conducted physical verification without the petitioner’s authorised representative remaining present. Even the notice of inspection for which SCN was issued had not been sent to the petitioner. Moreover, the petitioner owed no tax or cess. Therefore, the Court instructed the petitioner to submit an application for the revocation of registration cancellation, and that application was to be decided by the appropriate official by issuing a spoken order.

Judiciary Detail

HON’BLE MR. JUSTICE RAJIV SHAKDHER

HON’BLE MS. JUSTICE TARA VITASTA GANJU

[Physical Hearing/Hybrid Hearing (as per request)]

Counsel Detail

Counsel for Appellant: Mrs Anjali Jha Manish

Counsel for Respondent: Mr Sameer Vashisht and Ms Sanjana Nangia

CURIL TRADEX PVT. LTD vs COMMISSIONER

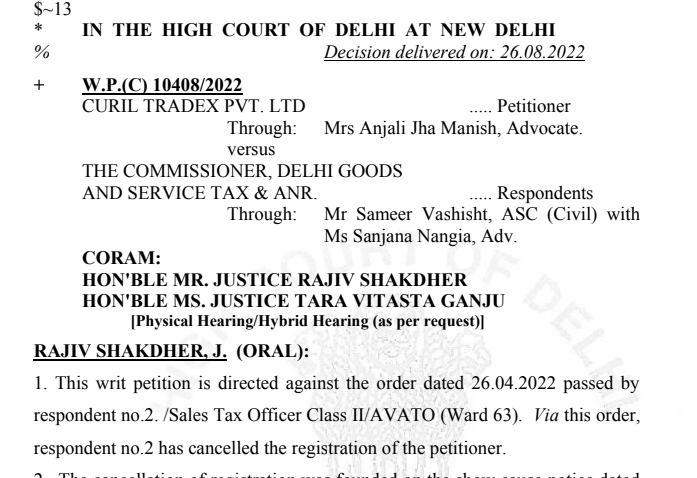

IN THE HIGH COURT OF DELHI AT NEW DELHI

+ W.P.(C) 10408/2022

CURIL TRADEX PVT. LTD ….. Petitioner

Through: Mrs Anjali Jha Manish, Advocate.

versus

THE COMMISSIONER, DELHI GOODS

AND SERVICE TAX & ANR. ….. Respondents

Through: Mr Sameer Vashisht, ASC (Civil) with

Ms Sanjana Nangia, Adv.

CORAM:

HON’BLE MR. JUSTICE RAJIV SHAKDHER

HON’BLE MS. JUSTICE TARA VITASTA GANJU

[Physical Hearing/Hybrid Hearing (as per request)]

Leave a Reply