ITR Filing Guidelines for AY 2026-27: Essential Guide for Salaried Employees, Senior Citizens, Freelancers and Small Businesses

Filing an Income Tax Return for Assessment Year 2026-27 needs more care than earlier years because the Income Tax Department has introduced important changes in ITR reporting, especially in ITR-1 and ITR-4. These changes directly affect salaried employees, pensioners, senior citizens, freelancers, consultants, small traders and service providers.

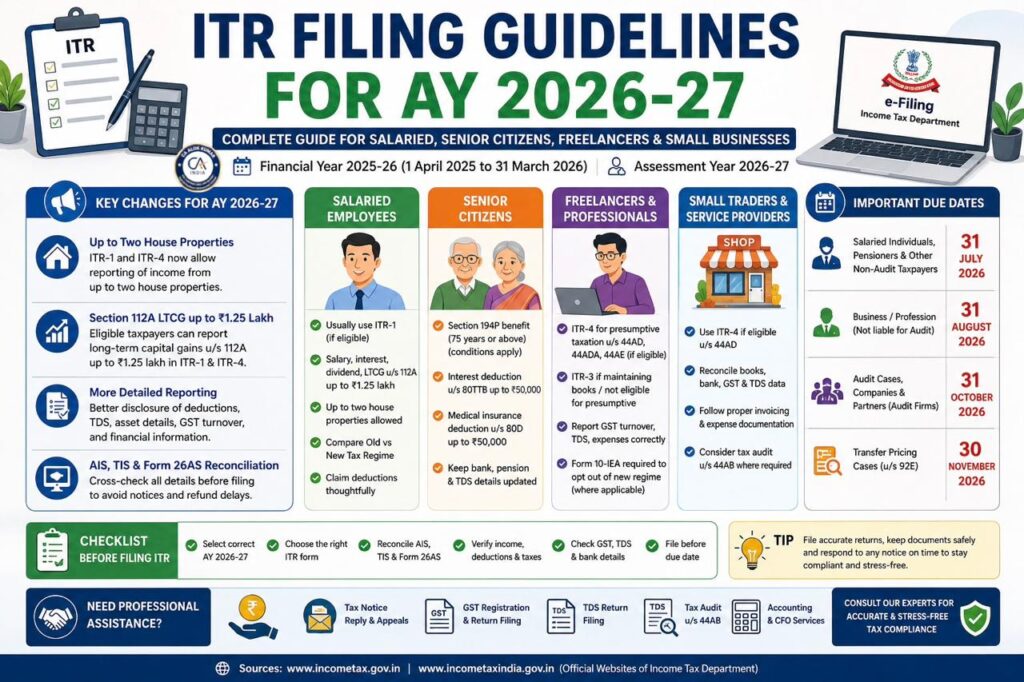

The most important starting point is simple: AY 2026-27 relates to income earned during FY 2025-26, that is, income from 1 April 2025 to 31 March 2026. The Income Tax Department’s official transition FAQ clarifies that income for FY 2025-26 will be filed for Assessment Year 2026-27 under the Income-tax Act, 1961, even though filing may happen after the Income-tax Act, 2025 comes into force.

Taxpayers who need professional help may use our dedicated ITR filing for AY 2026-27 service page. For taxpayers based in Delhi NCR, our ITR filing in Dwarka, Delhi page covers salaried employees, freelancers, traders, professionals, HNIs, HUFs, NRIs and small businesses; the page was verified as live.

Table of Contents

- What is AY 2026-27?

- Key changes in ITR forms for AY 2026-27

- ITR filing guidelines for salaried employees

- ITR filing guidelines for senior citizens

- ITR filing guidelines for freelancers and small businesses

- Reporting deductions, expenses and capital gains

- ITR Filing Due dates for AY 2026-27

- Checklist before filing ITR

- FAQs

- Final takeaway

ITR Filing Guidelines for AY 2026-27: What Has Changed?

For AY 2026-27, the Income Tax Department has enabled ITR utilities in phases. The official e-filing portal shows that online filing and Excel utilities for ITR-1 and ITR-4 were enabled on 15 May 2026, offline utilities for ITR-1 and ITR-4 were enabled on 20 May 2026, ITR-2 utilities were enabled in May 2026, and ITR-3 online filing and offline utility were enabled in June 2026.

The Income Tax Department also announced availability of utilities through its official social media handle on X/Twitter, including posts relating to ITR-1, ITR-4 and ITR-3 for AY 2026-27. The portal latest-news page should still be treated as the primary source for filing availability.

The key practical changes are as follows.

1. ITR-1 Now Allows Up to Two House Properties

The official ITR-1 form for AY 2026-27 states that it is for eligible resident individuals having total income up to ₹50 lakh from salary, two house properties, other sources, long-term capital gains under Section 112A up to ₹1.25 lakh and agricultural income up to ₹5,000.

This is a major relief for salaried employees and pensioners who own two houses but otherwise remain eligible for ITR-1. However, ITR-1 should not be used where the taxpayer has business income, foreign assets, foreign income, unlisted equity shares, directorship in a company, brought-forward losses, complex capital gains or other disqualifying items.

2. ITR-4 Now Covers More Practical Small-Business Situations

The official ITR-4 form for AY 2026-27 applies to eligible resident individuals, HUFs and firms other than LLPs having total income up to ₹50 lakh and business or professional income computed under Section 44AD, Section 44ADA or Section 44AE, along with permitted Section 112A capital gains up to ₹1.25 lakh.

For small businesses and professionals using presumptive taxation, ITR-4 is useful but not compulsory. The official Income Tax guidance clarifies that ITR-4 is a simplified return form to be used at the option of an eligible assessee declaring income on a presumptive basis under Section 44AD, 44ADA or 44AE.

Freelancers, consultants and traders who are unsure whether they should choose ITR-4 or ITR-3 may review our professional ITR filing for business and professionals support page.

3. Section 112A LTCG up to ₹1.25 Lakh Can Be Reported in ITR-1 and ITR-4

For AY 2026-27, eligible taxpayers can report long-term capital gains under Section 112A up to ₹1.25 lakh in ITR-1 or ITR-4, subject to other eligibility conditions. Section 112A generally covers listed equity shares, units of equity-oriented mutual funds and units of business trusts where prescribed conditions are satisfied. The official ITR-1 and ITR-4 forms both mention this threshold.

This does not mean all capital gains can be reported in ITR-1 or ITR-4. If there are short-term capital gains, long-term capital gains above the permitted threshold, property capital gains, foreign assets, business capital gains or losses to be carried forward, the taxpayer may need ITR-2 or ITR-3.

4. Two-House-Property Reporting Requires More Details

ITR-4 for AY 2026-27 specifically provides fields for house property details including address, co-owner details, let-out/self-occupied/deemed let-out classification, tenant PAN/Aadhaar/TAN where applicable, unrealised rent, municipal taxes, annual value, interest on borrowed capital and property-wise computation. The form also says that details are to be filled separately for each property up to two properties.

This means taxpayers should not treat house property reporting casually. Home loan interest, rental income, municipal tax, co-owner share and tenant details must be correctly reported.

ITR Filing Guidelines for Salaried Employees

Most salaried employees will generally begin by checking eligibility for ITR-1. A salaried employee may use ITR-1 where he or she is a resident individual, not ordinarily resident cases are excluded, total income does not exceed ₹50 lakh, income is from salary or pension, up to two house properties, other sources, permitted Section 112A LTCG up to ₹1.25 lakh and agricultural income up to ₹5,000.

However, salaried employees should not file only on the basis of Form 16. Before filing, they should reconcile Form 16, AIS, TIS, Form 26AS, salary slips, bank interest certificates, dividend income, mutual fund statements and capital gain reports. The Income Tax Department’s senior-citizen guidance also explains that AIS may contain tax deducted or collected, SFT information, tax payments, demand/refund and other information received by the Department.

For salaried taxpayers, common reporting areas include:

- Gross salary, taxable allowances and perquisites

- Standard deduction

- HRA exemption, where applicable

- Interest from savings bank and fixed deposits

- Dividend income

- Income from one or two house properties

- Capital gains under Section 112A up to eligible limit

- Deductions under Section 80C, 80D, 80CCD, 80G, 80TTA or 80TTB, where applicable

- Old regime versus new regime comparison

A taxpayer who receives a notice because of AIS mismatch, TDS mismatch, high-value transaction or deduction-related issue may need professional income tax demand notice response or faceless assessment representation. Both pages were verified as live.

ITR Filing Guidelines for Senior Citizens

Senior citizens must be careful about pension, bank interest, medical deductions, TDS and return-filing exemption rules.

Section 194P Relief for Senior Citizens Aged 75 Years or More

Section 194P provides conditional relief to certain resident senior citizens aged 75 years or more. The official Income Tax guidance states that a senior citizen aged 75 or above is not required to file return of income if income consists only of pension income and interest income from an account maintained with the specified bank, and the specified bank computes total income and deducts tax after considering Chapter VI-A deductions and Section 87A rebate.

This relief is not automatic for every senior citizen. A senior citizen with rental income, capital gains, dividend income, foreign assets, refund claim, interest from other banks or any other income outside the specified conditions should review return-filing requirements carefully.

Section 80TTB, Medical Insurance and Medical Expenditure

Senior citizens should correctly report bank interest and claim eligible deductions only where the selected tax regime permits them. The official Income Tax guidance states that Section 80TTB allows senior citizens deduction up to ₹50,000 on interest earned from deposits with banks, post offices or co-operative banks. It also explains the higher Section 80D limit of ₹50,000 for medical insurance premium and Section 80DDB deduction up to ₹1 lakh for specified disease treatment in senior-citizen cases.

Senior citizens should keep pension certificate, bank interest certificate, Form 16, Form 16A, medical insurance receipts, medical expenditure records and deduction documents safely.

For senior citizens in Delhi NCR, professional assistance may be routed through ITR filing in Dwarka, Delhi, particularly where pension, interest, capital gains, property income or refund claims are involved.

ITR Filing Guidelines for Freelancers, Consultants, Small Traders and Service Providers

Freelancers and small businesses should first decide whether they are eligible for presumptive taxation and ITR-4, or whether ITR-3 is required.

Presumptive Taxation Under Section 44AD and Section 44ADA

ITR-4 contains detailed fields for presumptive income under Section 44AD and Section 44ADA. For Section 44AD, the ITR-4 form refers to gross turnover or receipts generally limited to ₹2 crore, with extension to ₹3 crore where cash and non-prescribed modes are within the specified 5% condition. It also provides presumptive income at 6% for eligible banking/electronic receipts and 8% for cash/other receipts.

For Section 44ADA professionals, ITR-4 refers to gross receipts generally limited to ₹50 lakh, with extension to ₹75 lakh where cash and non-prescribed receipts are within the 5% condition. The form computes presumptive income at 50% of gross receipts or higher amount claimed.

Where income is reported below the presumptive percentage, or where conditions are not satisfied, tax audit and a different ITR may be required. Taxpayers facing such issues should review tax audit under Section 44AB. That service page was verified as live.

GST Turnover and Business Reporting

ITR-4 requires reporting of GSTIN and annual value of outward supplies as per GST returns. This is important for freelancers, traders and small service providers registered under GST. Business turnover in books, bank accounts, GST returns, TDS records and ITR should be reconciled before filing. The ITR-4 form specifically asks for GSTIN-wise annual outward supplies as per GST returns.

For registered businesses, GST registration and return filing should be reconciled with income-tax reporting. That page was verified as live and covers GST registration, return filing and compliance management.

TDS Reporting for Freelancers

Freelancers and consultants often receive Form 16A for professional fees. ITR-4 contains Schedule TDS-2 for TDS on income other than salary and requires corresponding receipts to be offered for tax while claiming TDS credit.

If professional fees, commission or contract receipts are subject to TDS, the freelancer should reconcile invoices, bank credits, Form 16A, Form 26AS, AIS and GST turnover. For quarterly TDS compliance or TDS mismatch, taxpayers may use TDS filing and notice reply services, which was verified as live.

Expense Claims: Presumptive Taxation vs Regular Books

Freelancers, traders and small service providers must understand the difference between presumptive taxation and actual-profit computation.

Under presumptive taxation, income is computed at the prescribed percentage or a higher declared amount. Routine business expenses are not separately claimed in the same manner as regular books-based computation.

Where the taxpayer maintains regular books and files ITR-3, genuine business expenses may be claimed if they are wholly and exclusively for business or profession and are supported by records. Common deductible business expenses may include office rent, internet, software subscription, professional fees, staff cost, payment gateway charges, bank charges, business travel, depreciation and accounting expenses.

Personal expenses should not be claimed as business expenses. Mixed-use expenses should be allocated carefully. Businesses needing regular bookkeeping, MIS and compliance support may consider virtual CFO and accounting outsourcing, which was verified as a live service page.

Old Tax Regime, New Tax Regime and Form 10IEA

The new tax regime is the default regime. ITR-4 for AY 2026-27 specifically states that the old regime can be chosen by opting out of the new regime through Form 10IEA, and the option should be exercised on or before the due date for filing return under Section 139(1).

For salaried employees without business income, regime selection is comparatively flexible. For taxpayers having business or professional income, the decision requires more caution because opting in and out may have restrictions. Freelancers and small businesses should compare deductions, presumptive income, tax liability, advance tax, TDS and compliance history before selecting the regime.

Due Dates for AY 2026-27

The official transition FAQ confirms that ITR for income from 1 April 2025 to 31 March 2026 will be filed for AY 2026-27 with due dates of 31 July 2026, 31 August 2026, 31 October 2026 or 30 November 2026, as applicable.

The Income Tax Department’s return-of-income guidance states that the due date for a person engaged in business other than a company whose accounts are not required to be audited is 31 August of the assessment year, audit cases other than transfer-pricing cases are generally 31 October, and transfer-pricing cases under Section 92E are 30 November.

| Taxpayer Category | Due Date for AY 2026-27 |

|---|---|

| Salaried individuals, pensioners and other non-audit taxpayers | 31 July 2026 |

| Business/profession taxpayers not required to get accounts audited | 31 August 2026 |

| Audit cases, including companies and applicable partners | 31 October 2026 |

| Transfer pricing cases requiring Form 3CEB | 30 November 2026 |

The last date for belated return for AY 2026-27 is generally 31 December 2026, unless assessment is completed earlier. The official FAQ also states that delayed filing fee under Section 234F is ₹1,000 where total income does not exceed ₹5 lakh and ₹5,000 in other cases.

Practical Checklist Before Filing ITR for AY 2026-27

Before filing, taxpayers should complete the following checklist:

- Select AY 2026-27 correctly.

- Confirm whether ITR-1, ITR-2, ITR-3 or ITR-4 applies.

- Reconcile Form 16, Form 16A, AIS, TIS and Form 26AS.

- Compare old tax regime and new tax regime.

- Check Form 10IEA requirement where business or professional income exists.

- Report all bank accounts except dormant accounts where permitted by the form.

- Report interest, dividend and capital gains correctly.

- For two house properties, verify ownership share, tenant details, rent, municipal taxes and loan interest.

- For freelancers, reconcile invoices, bank credits, TDS, GST turnover and books.

- Do not claim unsupported personal expenses as business expenses.

- Verify advance tax, self-assessment tax, TDS and TCS.

- Validate refund bank account.

- Preserve proofs for deductions, medical claims, donations and housing loan interest.

- Review AIS mismatch before filing.

- File before the due date to avoid late fee and loss-related restrictions.

FAQs on ITR Filing Guidelines for AY 2026-27

1. Which financial year is covered by AY 2026-27?

AY 2026-27 covers income earned during FY 2025-26, from 1 April 2025 to 31 March 2026. The official transition FAQ clarifies that this return is governed by the Income-tax Act, 1961.

2. Can salaried employees with two house properties file ITR-1?

Yes, eligible resident individuals can file ITR-1 with income from up to two house properties, subject to all other ITR-1 eligibility conditions.

3. Can freelancers file ITR-4 for AY 2026-27?

Freelancers may file ITR-4 only if they are eligible for presumptive taxation under Section 44ADA or other applicable presumptive provisions and satisfy all ITR-4 conditions. Otherwise, ITR-3 may be required.

4. Is Section 112A capital gain allowed in ITR-1 and ITR-4?

Yes, eligible Section 112A long-term capital gains up to ₹1.25 lakh may be reported in ITR-1 or ITR-4, subject to eligibility. Other capital gains may require ITR-2 or ITR-3.

5. Do senior citizens above 75 years always need to file ITR?

No. Certain resident senior citizens aged 75 years or more may be exempt from filing ITR if they satisfy Section 194P conditions, including only pension and interest income from the specified bank and tax deduction by that bank.

6. What is the due date for salaried employees for AY 2026-27?

For salaried individuals and pensioners not covered by audit or other special provisions, the due date is generally 31 July 2026.

7. What is the due date for small businesses not covered by tax audit?

For a person engaged in business other than a company whose accounts are not required to be audited, the due date is 31 August 2026 for AY 2026-27.

Final Takeaway

The ITR Filing Guidelines for AY 2026-27 show that simplified ITR forms have become more useful but also more data-driven. Salaried taxpayers can benefit from ITR-1 if eligible, especially with the new two-house-property reporting. Senior citizens should review Section 194P, 80TTB, pension and interest reporting carefully. Freelancers, consultants, small traders and service providers should decide between ITR-4 presumptive taxation and ITR-3 regular business reporting only after reconciling invoices, GST, TDS, AIS and books.

For accurate return filing, taxpayers may use professional ITR filing for AY 2026-27. Delhi NCR taxpayers may also use ITR filing in Dwarka, Delhi. Businesses with GST or TDS issues should also review GST registration and return filingand TDS filing and notice reply services.

Disclaimer: This article is for general information and educational purposes. Taxpayers should obtain case-specific professional advice before filing returns or responding to any notice.

Leave a Reply