Supreme Court Remands JAO vs FAO Reassessment Cases After Section 147A Amendment

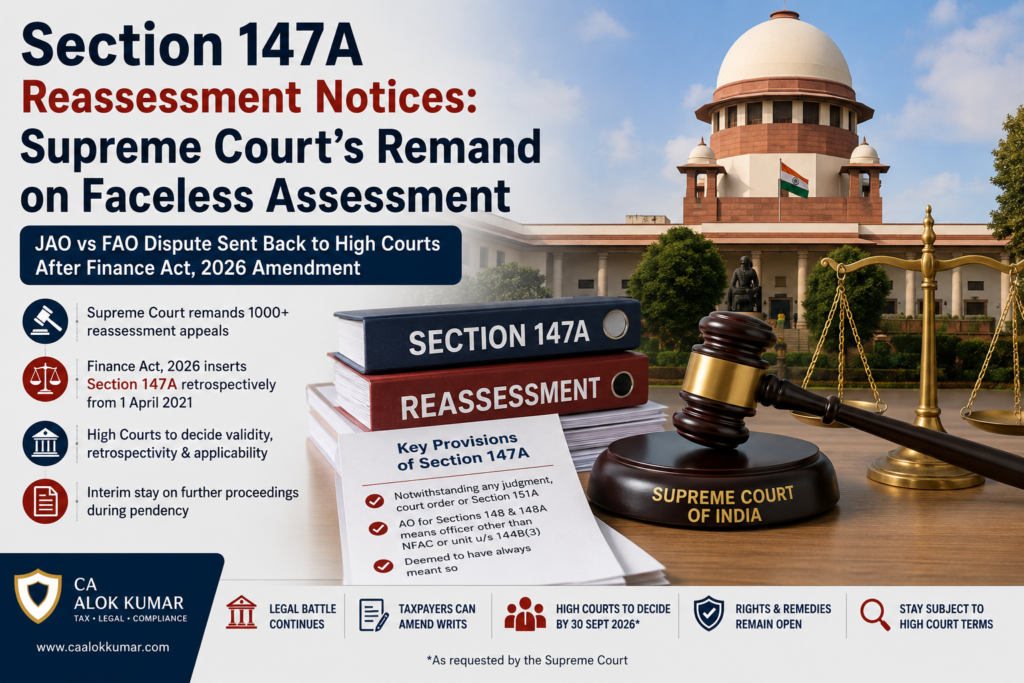

Section 147A reassessment notices have now become an important litigation issue after the Supreme Court’s order in Income Tax Officer, Ward 2(1), Chandigarh & Ors. v. Tej Partap Singh. The Supreme Court disposed of a large batch of reassessment appeals and remitted the matters to the respective High Courts after Parliament inserted Section 147A through the Finance Act, 2026.

The Supreme Court has not finally decided the constitutional validity, retrospectivity, scope or applicability of Section 147A. Instead, it has directed the High Courts to examine the matter afresh in the light of the new statutory provision. The official Gazette text of the Finance Act, 2026 states that Section 147A is deemed to have been inserted with effect from 1 April 2021 and clarifies the meaning of “Assessing Officer” for Sections 148 and 148A.

Table of Contents

- Background of the JAO vs FAO reassessment dispute

- What Section 147A says after Finance Act, 2026

- What the Supreme Court decided in Tej Partap Singh

- What remains open before High Courts

- Practical impact for taxpayers

- Action points for reassessment notice cases

- FAQs on Section 147A reassessment notices

Background of the JAO vs FAO Reassessment Dispute

The controversy started after the Finance Act, 2021 changed the reassessment framework under Sections 147 to 151 of the Income-tax Act, 1961. Section 148A introduced a pre-notice procedure before issuing a reassessment notice under Section 148.

Under Section 148A, the Assessing Officer is generally required to provide the assessee an opportunity of being heard, consider the reply, and pass an order before issuing a notice under Section 148. The Income Tax Department’s official section page describes Section 148A as the provision for conducting inquiry and providing opportunity before issue of notice under Section 148. (Etds)

The Central Government also notified the e-Assessment of Income Escaping Assessment Scheme, 2022 through CBDT Notification No. 18/2022 dated 29 March 2022 under Section 151A. The notification relates to the faceless mechanism for reassessment proceedings. (Etds)

This led to a major dispute: whether reassessment notices and Section 148A orders should be issued only through the faceless mechanism, or whether the Jurisdictional Assessing Officer could also issue them. Several taxpayers challenged notices issued by JAOs. Some High Courts accepted the taxpayer’s argument, while other High Courts took a different view. The Supreme Court noted this divergence while remitting the matter. (Indian Kanoon)

For taxpayers already facing proceedings, proper faceless assessment representation becomes critical because the dispute is no longer limited to a technical jurisdiction issue alone.

What Section 147A Says After Finance Act, 2026

The Finance Act, 2026 inserted Section 147A into the Income-tax Act, 1961 with retrospective effect from 1 April 2021. The provision states that, notwithstanding any judgment, court order, Section 151A, or any scheme framed under Section 151A, the Assessing Officer for the purposes of Sections 148 and 148A shall mean, and shall always be deemed to have meant, an Assessing Officer other than the National Faceless Assessment Centre or any assessment unit referred to in Section 144B(3).

In simple terms, Parliament has attempted to clarify retrospectively that the JAO was competent for issuing notices and passing orders under Sections 148 and 148A, notwithstanding the faceless reassessment scheme.

This amendment has changed the legal landscape in JAO vs FAO reassessment cases. It is the main reason why the Supreme Court did not finally decide the old statutory dispute and instead sent the matters back to the High Courts.

What the Supreme Court Decided in Tej Partap Singh

In Income Tax Officer, Ward 2(1), Chandigarh & Ors. v. Tej Partap Singh, the Supreme Court observed that several High Courts had quashed Section 148A(d) orders and consequential Section 148 notices mainly because they were issued by JAOs instead of through the faceless mechanism. The Court also noted that other High Courts had taken a contrary view and upheld the authority of the JAO. (Indian Kanoon)

Since Section 147A had been inserted with retrospective effect, the Supreme Court held that the foundation of the High Court judgments had changed. Therefore, the Court set aside the impugned High Court judgments on this limited ground and remitted the matters to the respective High Courts for fresh consideration. (Indian Kanoon)

The Court granted liberty to assessees to amend their writ petitions within four weeks from uploading of the order to challenge Section 147A, or any connected or consequential provision. The Revenue was also granted liberty to file written submissions and affidavits within three weeks thereafter. (Indian Kanoon)

What the Supreme Court Did Not Decide

The most important point is that the Supreme Court did not uphold Section 147A on merits. It expressly clarified that it had not expressed any opinion on the validity, scope, effect, retrospectivity or applicability of the amended provisions. All such questions have been left open for the High Courts. (Indian Kanoon)

Therefore, taxpayers should not assume that every Section 148 notice issued by a JAO has automatically become valid. At the same time, they should also not assume that all such notices will automatically fail after remand.

The litigation has now moved to the next stage. High Courts will examine the amended law, constitutional arguments, retrospective operation, limitation, sanction approval, natural justice and factual defects in each case.

Interim Stay and High Court Timeline

The Supreme Court directed that during the pendency of the writ petitions before the High Courts, there shall be an interim stay of further assessment or reassessment proceedings pursuant to the impugned notices, subject to such terms and conditions as may be imposed by the respective High Courts. The High Courts were requested to decide the matters preferably by 30 September 2026. (Indian Kanoon)

This interim protection is significant, but it should be read carefully. The stay is linked to the pending writ petitions and is subject to the terms and conditions imposed by the concerned High Court.

Practical Impact for Taxpayers

The Supreme Court’s order is procedural, but its practical impact is substantial. Taxpayers who had obtained favourable High Court orders only on the JAO-versus-FAO jurisdiction ground may now need to contest the matter afresh.

Taxpayers with pending writ petitions should review whether their pleadings need amendment to specifically challenge Section 147A, its retrospective effect, and connected provisions.

Taxpayers should preserve the following documents:

- Section 148A(b) notice

- Information or material relied upon by the department

- Reply filed by the assessee

- Section 148A(d) order

- Section 148 notice

- Approval or sanction under Section 151

- Limitation working under Section 149

- Copy of writ petition, interim order and High Court pleadings

- Assessment or reassessment proceedings, if already initiated

Where a demand has already been raised or may arise after reassessment, taxpayers should avoid casual portal replies and seek proper income tax demand notice response support before accepting, disputing or paying any demand.

Issues Taxpayers Should Examine Beyond JAO vs FAO

After insertion of Section 147A, the issue is no longer limited to whether the notice was issued by a JAO or FAO. Taxpayers and professionals must also examine:

- Whether there was valid “information suggesting escapement of income”

- Whether the Section 148A(b) notice supplied adequate material

- Whether the assessee’s reply was properly considered

- Whether the Section 148A(d) order shows application of mind

- Whether sanction under Section 151 was validly obtained

- Whether the notice is within limitation under Section 149

- Whether the case is based merely on suspicion or borrowed satisfaction

- Whether reassessment is barred by change of opinion

- Whether the retrospective amendment can constitutionally cure the defect

In many cases, reassessment disputes also arise because the original return was wrongly filed, income was incorrectly reported, or a wrong form was used. Where applicable, taxpayers may also need a review of ITR-B filing, return disclosure, AIS/TIS reporting and supporting documentation.

Can ITR-U Help in Reassessment Cases?

An updated return under Section 139(8A) may help in limited situations where the law permits correction before proceedings reach a restrictive stage. However, once reassessment proceedings or specific statutory bars apply, ITR-U may not be available in every case.

Therefore, taxpayers should first review the notice status, assessment year, limitation period, and statutory restrictions before considering ITR-U updated return filing. A wrong ITR-U strategy may create further complications in a reassessment matter.

NRI and Foreign Remittance Cases

Reassessment notices may also arise in cases involving foreign assets, NRI income, sale of property, remittance from NRO to NRE accounts, or mismatch in foreign remittance reporting. In such cases, the taxpayer may need reconciliation of Form 26AS, AIS, bank credits, capital gains computation and remittance documentation.

Where funds are being remitted abroad, taxpayers may also need professional assistance for Form 145-146 CA certificate for foreign remittance, depending on the facts of the case.

Practical Takeaway

The Supreme Court has not validated every reassessment notice issued by a JAO. It has also not accepted every taxpayer challenge. It has only recognised that Finance Act, 2026 has changed the statutory position and that High Courts must now decide the controversy afresh.

The key takeaway is simple: Section 147A reassessment notices require a fresh, fact-specific and legally supported response. Taxpayers should not rely only on the earlier JAO vs FAO argument. They should examine jurisdiction, limitation, approval, material relied upon, natural justice, factual correctness and constitutional grounds.

For taxpayers estimating potential tax exposure, interest or relief issues, an income tax relief calculator may be useful as a preliminary tool, but final tax and litigation strategy should be based on detailed facts and legal review.

FAQs on Section 147A Reassessment Notices

1. Did the Supreme Court uphold Section 147A?

No. The Supreme Court expressly stated that it has not expressed any opinion on the validity, scope, effect, retrospectivity or applicability of the amended provisions. These issues have been left open for the High Courts. (Indian Kanoon)

2. Are all JAO-issued reassessment notices now valid?

Not automatically. Section 147A supports the Revenue’s jurisdictional argument, but taxpayers can still challenge reassessment notices on limitation, sanction, natural justice, non-application of mind, factual defects and constitutional grounds.

3. What is the relevance of Section 151A faceless scheme now?

Section 151A and the faceless reassessment scheme remain relevant because Section 147A itself refers to Section 151A and any scheme framed under it. The High Courts will now examine the effect of Section 147A in the context of the faceless scheme and earlier judicial decisions.

4. What should taxpayers with pending writ petitions do?

They should immediately review whether their writ petitions need amendment to challenge Section 147A and connected provisions. The Supreme Court granted liberty for amendment within the specified timeline. (Indian Kanoon)

5. Is reassessment stayed after the Supreme Court order?

The Supreme Court directed interim stay of further assessment or reassessment proceedings pursuant to the impugned notices during pendency before the High Courts, subject to terms and conditions imposed by those High Courts. (Indian Kanoon)

6. What is the significance of 30 September 2026?

The Supreme Court requested the High Courts to decide the remanded matters preferably by 30 September 2026. (Indian Kanoon)

Leave a Reply