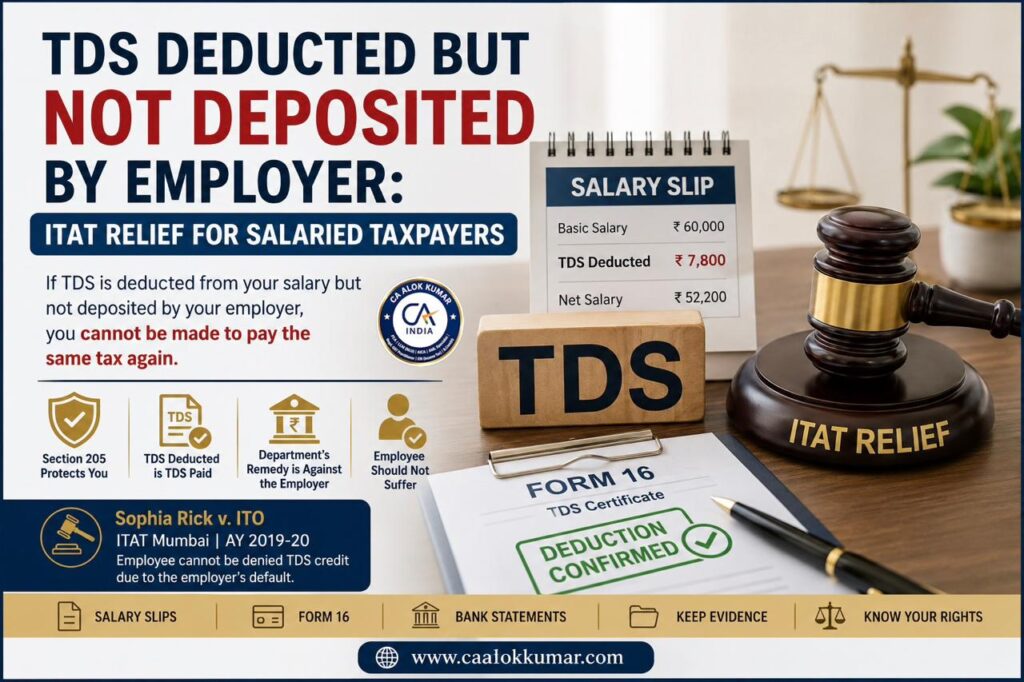

When TDS deducted but not deposited by employer does not appear in Form 26AS, salaried taxpayers often face a difficult situation: the employer has already reduced tax from salary, but the Income Tax Department’s CPC system may still raise a demand because the corresponding credit is missing. A recent Mumbai ITAT ruling in Sophia Rick v. ITO has again reinforced an important principle: an employee should not be made to pay the same tax again merely because the employer failed to deposit TDS with the Government. The Tribunal directed the Assessing Officer to verify salary slips, Form 16, bank statements and supporting records, and allow full TDS credit if deduction from salary is established.

Table of Contents

- What happened in Sophia Rick v. ITO

- Why Form 26AS mismatch led to tax demand

- Section 205 protection when TDS is already deducted

- Importance of salary slips, Form 16 and bank statements

- What salaried taxpayers should do after receiving a CPC demand

- Practical implications for employees and employers

- FAQs

What happened in Sophia Rick v. ITO

The case concerned Assessment Year 2019-20. The taxpayer, an employee of Trimax IT Infrastructure & Services Ltd, filed her income tax return declaring income of about ₹18.41 lakh and claimed TDS credit of ₹3,91,241. However, while processing the return under section 143(1), the CPC allowed credit of only ₹79,030 because the balance TDS was not reflected in Form 26AS. This led to a demand of more than ₹3 lakh.

The mismatch arose because the employer had allegedly deducted tax from salary but failed to remit the full amount to the Government. The employee pursued rectification before CPC for several years. When rectification did not resolve the issue, she filed an appeal. The first appellate authority dismissed the appeal as time-barred, but the ITAT accepted that the delay was bona fide because the taxpayer had been diligently pursuing rectification proceedings.

Why Form 26AS mismatch led to tax demand

Form 26AS is a tax credit statement generated from information reported by deductors. If an employer deducts TDS but does not deposit it or does not correctly file the TDS return, the employee’s Form 26AS may not show the full credit. In automated CPC processing, the credit claimed in the return is compared with available system records. A mismatch may therefore result in partial denial of TDS credit and a demand notice.

The Mumbai ITAT did not treat Form 26AS as the only decisive record. The Tribunal considered whether the employee could prove actual deduction of TDS from salary. According to the reported order, the taxpayer produced salary slips, Form 16, bank statements and other documents showing that tax was deducted and only net salary was credited to her bank account.

Section 205 protection when TDS is already deducted

The legal foundation of this relief lies in section 205 of the Income-tax Act, 1961. The provision states that where tax is deductible at source, the assessee shall not be called upon to pay the tax himself to the extent to which tax has been deducted from that income. (Etds)

This means that once an employee establishes that tax was actually deducted from salary, the Revenue’s remedy is generally against the defaulting deductor, not against the employee. Section 201 separately deals with consequences for a person who fails to deduct or, after deducting, fails to pay TDS. The official Income Tax Department guidance on section 201 also recognises interest consequences for failure to deduct or delay in payment of TDS. (Etds)

Section 199 provides the general rule for credit of tax deducted and paid to the Central Government, but courts and tribunals have repeatedly read section 199 harmoniously with section 205 so that an innocent deductee is not subjected to double recovery merely because of deductor default. (Etds)

Judicial precedents supporting the employee

The principle is not new. In Devarsh Pravinbhai Patel v. ACIT, the Gujarat High Court dealt with a similar situation where the employer had deducted TDS but failed to deposit it. The Court held that the Department could not deny the benefit of tax deducted at source to the employee and could recover the amount from the deductor. (itatonline.org)

The Supreme Court’s 2026 order in Income Tax Assessing Officer v. Shobhan Shantilal Doshi is also relevant. The Supreme Court noted that the Revenue had not challenged the relief granted to the taxpayer on merits; the appeal was confined to directions requiring CBDT software changes. The Court set aside those software directions, but did not disturb the taxpayer-specific relief. (Supreme Court of India)

The Mumbai ITAT’s approach in Sophia Rick therefore fits within a consistent judicial line: if TDS deduction from income is established by reliable evidence, the deductee should not be made to suffer for the deductor’s default.

What documents can prove TDS deduction?

For salaried employees, documentation is critical. The Sophia Rick ruling is useful because the ITAT did not grant credit blindly. It directed the Assessing Officer to verify the taxpayer’s claim and allow credit if the evidence proves deduction.

Employees facing similar issues should preserve:

Salary slips showing monthly TDS deduction.

Form 16 issued by the employer.

Bank statements showing net salary credit.

Employment contract, appointment letter, resignation or relieving records.

Email communication with employer about TDS, Form 16 or correction.

Form 26AS, AIS and TIS downloads for the relevant year.

Copy of rectification applications and CPC responses.

Copy of demand notice under section 143(1) or outstanding demand portal screenshot.

What salaried taxpayers should do after receiving a CPC demand

A taxpayer should not ignore a demand merely because the employer is at fault. The correct approach is to respond with evidence.

First, compare ITR, Form 16, salary slips, AIS/TIS and Form 26AS. Second, approach the employer and request correction of the TDS return and deposit of tax. Third, file rectification under section 154 wherever the intimation is capable of correction. Fourth, if the demand is shown under “Response to Outstanding Demand”, submit a reasoned response with documentary proof. Fifth, if rectification fails or relief is denied, consider appeal within limitation or seek condonation with evidence of bona fide pursuit of remedy.

Practical implications for employers

Employers should treat this ruling as a compliance warning, not as relief. Failure to deposit TDS after deduction can expose the employer to interest, penalty, prosecution risk and recovery proceedings. Employers must ensure timely TDS deposit, correct quarterly TDS return filing, Form 16 issuance, and reconciliation of Form 24Q with employee payroll records.

Practical takeaway

The ruling is a strong reminder that TDS deducted but not deposited by employer should not result in double tax recovery from the employee. However, relief depends on proof. Salaried taxpayers should not rely only on Form 26AS. They must preserve salary slips, Form 16, bank records and correspondence to prove that tax was actually deducted from salary.

FAQs

1. Can the Income Tax Department deny TDS credit if my employer has not deposited TDS?

The Department may initially deny credit during CPC processing if the amount is not reflected in Form 26AS. However, section 205 protects the taxpayer to the extent tax has actually been deducted from income. The taxpayer must prove deduction through records. (Etds)

2. Is Form 26AS final proof of TDS credit?

Form 26AS is important but not always conclusive in employer default cases. If TDS was actually deducted but not properly deposited or reported by the employer, salary slips, Form 16 and bank statements may support the employee’s claim.

3. What should I do if I receive a tax demand due to TDS mismatch?

File a response with supporting documents, pursue rectification where appropriate, and take appellate remedy if relief is not granted. Do not ignore the notice.

4. Can the Department recover TDS from the employer?

Yes. Section 201 deals with consequences where a person responsible for TDS fails to deduct or pay tax after deduction. (Etds)

5. Does this ruling automatically remove every TDS mismatch demand?

No. The Assessing Officer can verify whether TDS was actually deducted. Relief depends on documents and facts.

Leave a Reply