Introduction of Form 102 of Income Tax (Earlier Form 71 of Income Tax)

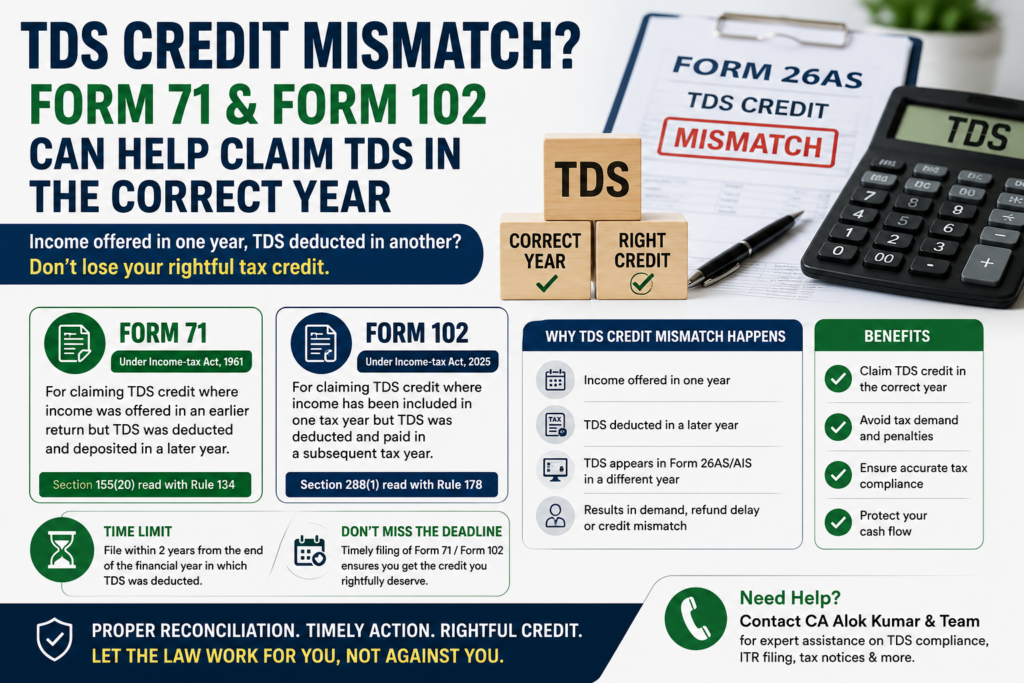

A common problem faced by taxpayers is that income is offered to tax in one financial year, but the related TDS is deducted and reflected in Form 26AS or AIS in a later year.

This creates a genuine hardship. The taxpayer has already disclosed the income, but the credit of tax deducted at source does not appear in the same year. This may lead to a tax demand, refund blockage, CPC mismatch, or repeated rectification issues.

To address this, the Income Tax framework provides a specific remedy. Under the Income-tax Act, 1961, the relevant form is Form 71. Under the Income-tax Act, 2025, the corresponding form is Form 102.

Taxpayers facing such mismatch may also require professional review of ITR filing, TDS compliance, or income tax demand notice response, depending on the status of processing or demand.

What is TDS Credit Mismatch?

A TDS credit mismatch occurs when the timing of income recognition and TDS deduction is different.

For example:

| Particulars | Year |

| Income offered to tax | FY 2024-25 |

| TDS deducted by payer | FY 2025-26 |

| TDS reflected in Form 26AS/AIS | AY 2026-27 |

| Correct year for TDS credit | AY 2025-26 |

This may happen in professional fees, government contracts, delayed invoices, property transactions, NRI transactions, salary arrears, or late TDS reporting by the deductor.

What is Form 71 of Income Tax?

Form 71 is an e-application used under section 155(20) of the Income-tax Act, 1961 read with Rule 134 of the Income-tax Rules, 1962. It is used where income was already offered to tax in an earlier return, but TDS was deducted and deposited in a subsequent financial year.

The official Income Tax Department page describes Form 71 as an e-application for claiming TDS credit where income was offered in an earlier return but TDS was deducted and deposited later. It also states that the form is linked with section 155(20) and Rule 134. (Etds)

What is Form 102 of Income Tax?

Form 102 is the corresponding form under the Income-tax Act, 2025. It applies under section 288(1), Table Sl. No. 11, read with Rule 178 of the Income-tax Rules, 2026.

The Income Tax Department’s Form 102 FAQ states that Form 102 is used for claiming TDS credit where income has been included in the return for a tax year, but TDS on that income was deducted and paid to the Central Government in a subsequent tax year.

The official Form Navigator also maps Form 102 under the 2026 Rules to Form 71 under the 1962 Rules, confirming that Form 102 is the successor form for this purpose.

When Should Form 71 or Form 102 Be Used?

Use Form 71 or Form 102 when:

The income has already been included in the return of income.

TDS was deducted in a later financial year or tax year.

The TDS credit is not available in the year in which the income was taxed.

The taxpayer wants the TDS credit in the correct year.

The same TDS credit has not been claimed in another year.

For taxpayers in Delhi NCR, a detailed reconciliation can be reviewed with a tax consultant in Dwarka, especially where the mismatch has already resulted in a tax demand.

Practical Examples

1. Professional Fees Booked in March, TDS Deducted in April

A consultant raises an invoice in March 2025 and offers the income in FY 2024-25. The client deducts TDS in April 2025. The income is taxed in AY 2025-26, but TDS appears in AY 2026-27.

Form 71 may be used to claim credit in AY 2025-26.

2. Government Contractor Bills

Government departments may process bills late. If a contractor recognises income on accrual basis in one year but TDS is deducted in a later year, Form 71 or Form 102 may help.

3. NRI Property Sale

In some cases, a seller may offer capital gains in the year of transfer, while the buyer deducts or deposits TDS later. This should be reviewed along with TDS on sale of property and NRI taxation and FEMA implications.

4. Salary Arrears or Delayed Employer Reporting

Where salary, allowance, arrears or perquisite income is disclosed in one year but employer TDS is reported later, Form 71/Form 102 may be relevant, subject to factual matching.

Time Limit for Filing

Form 71 is to be furnished within two years from the end of the financial year in which TDS was deducted at source, as stated on the Income Tax Department’s Form 71 page. (Etds)

The Form 102 FAQ similarly provides that Form 102 may be filed after TDS has been deducted but within two years from the end of the financial year in which such TDS was deducted and reported by the deductor.

| TDS Deducted During | Last Date |

| FY 2025-26 | 31 March 2028 |

| FY 2026-27 | 31 March 2029 |

| FY 2027-28 | 31 March 2030 |

Documents Required

Keep the following ready:

ITR acknowledgement of the year in which income was offered.

Computation of income.

Invoice, ledger, agreement or contract.

Form 26AS, AIS and TIS.

TDS certificate such as Form 16, 16A or 16B.

Deductor PAN/TAN details.

Reconciliation statement linking income and TDS.

CPC intimation or demand notice, if any.

Where the mismatch has already triggered scrutiny or adjustment, professional support for faceless assessment or tax litigation may be required.

How to File Form 71 or Form 102

Login to the Income Tax e-filing portal.

Select the relevant income tax form.

Enter taxpayer details, assessment year/tax year, income details and TDS particulars.

Verify whether the same income was already offered to tax.

Submit the form electronically using DSC or EVC, as applicable.

Rule 134 provides that Form 71 is to be furnished electronically, either under digital signature or through EVC, depending on the case. (Etds)

Common Mistakes to Avoid

Do not file Form 71/Form 102 merely because TDS is not visible due to deductor default.

Do not claim the same TDS in two years.

Do not use it if income was not offered to tax earlier.

Do not ignore wrong PAN/TAN reporting by the deductor.

Do not file without reconciliation between income and TDS.

Businesses should also review their TDS return filing process to avoid such mismatches in future.

Conclusion

Form 71 and Form 102 provide an important statutory remedy for taxpayers facing TDS credit mismatch. The key point is simple: if income was already taxed in one year, but TDS was deducted and reflected in a later year, the taxpayer may apply for credit in the correct year.

Timely filing, accurate reconciliation and proper documentation are essential. Where the mismatch has resulted in a tax demand, refund blockage or assessment query, expert assistance from an income tax services in Dwarka team may help avoid unnecessary litigation.

FAQs

What is Form 71 in income tax?

Form 71 is an e-application under section 155(20) of the Income-tax Act, 1961 for claiming TDS credit in the year in which income was offered to tax, where TDS was deducted in a later year.

What is Form 102 under the Income-tax Act, 2025?

Form 102 is the corresponding form under the Income-tax Act, 2025 for claiming TDS credit where income and TDS deduction fall in different years.

What is the time limit for Form 71?

The time limit is two years from the end of the financial year in which the TDS was deducted.

Can Form 71 be used for wrong PAN cases?

Generally, wrong PAN cases require deductor correction first. Form 71 is not a substitute for PAN/TDS return correction.

Can TDS credit be claimed twice?

No. Once credit is allowed in the correct year, it cannot be claimed again in another year.

Leave a Reply