GSTN E-Way Bill Update 2026: Ship-To GSTIN Mandatory and Voluntary Closure Facility from 1 August 2026

Introduction

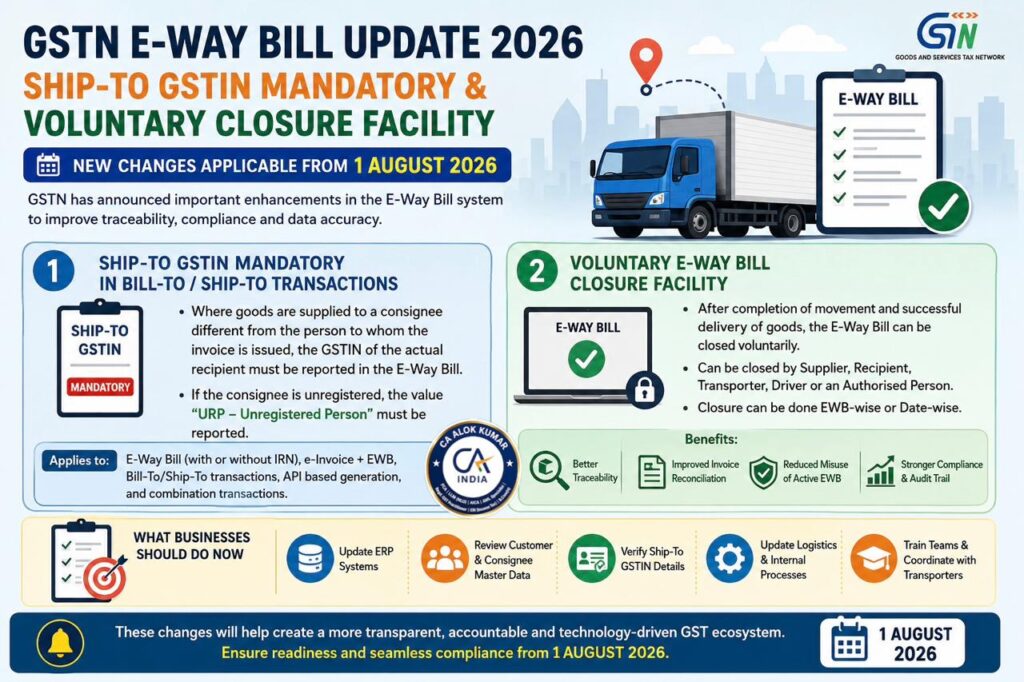

The Goods and Services Tax Network has announced important enhancements in the E-Way Bill system to improve traceability, accuracy of goods movement data and post-delivery reconciliation. The implementation of these changes has now been deferred to 1 August 2026, giving taxpayers, ERP vendors, GST Suvidha Providers, transporters and businesses additional time to update their systems and internal processes.

The two major changes are:

- Mandatory reporting of Ship-To GSTIN in Bill-To/Ship-To transactions.

- Introduction of a voluntary E-Way Bill closure facility after completion of goods movement.

These changes are highly relevant for manufacturers, traders, distributors, e-commerce sellers, logistics companies, transporters, warehouses, depots, consignment agents and businesses using ERP/API-based E-Way Bill generation.

What is the new E-Way Bill update?

The update relates to cases where the person billed in the invoice and the person actually receiving the goods are different.

This generally happens in Bill-To/Ship-To transactions, where:

- the invoice is issued to one GST-registered person;

- goods are delivered to another location or another consignee;

- the actual recipient may be a branch, project site, warehouse, customer, job worker, dealer or third-party consignee.

From 1 August 2026, where Ship-To details are provided and an E-Way Bill is required, the Ship-To GSTIN will become a mandatory data field.

Where the actual consignee is unregistered, the value “URP” will have to be reported in the Ship-To GSTIN field.

Meaning of Bill-To/Ship-To transaction

A Bill-To/Ship-To transaction is a supply arrangement where billing and delivery happen to different persons or locations.

Example

ABC Ltd. of Delhi places an order with a supplier in Haryana. ABC Ltd. instructs the supplier to deliver the goods directly to its project site or customer in Rajasthan.

In this case:

- Bill-To party: ABC Ltd., Delhi

- Ship-To party: Actual consignee/project site/customer in Rajasthan

- E-Way Bill requirement: Ship-To GSTIN or URP, as applicable, must be correctly reported

This reporting will help the GST system identify the actual movement of goods and reduce mismatches between invoice data and delivery details.

Ship-To GSTIN to become mandatory

The most important change is that the E-Way Bill system will require the GSTIN of the actual consignee in Bill-To/Ship-To cases.

This means businesses must ensure that the customer master, consignee master and delivery location records are correctly updated before generating E-Way Bills.

What should be reported?

| Situation | Reporting requirement |

| Ship-To party is GST registered | Report valid Ship-To GSTIN |

| Ship-To party is unregistered | Report “URP” |

| GSTIN is invalid | E-Way Bill may be rejected by system validation |

| Bill-To and Ship-To GSTIN are same in Bill-To/Ship-To transaction | Not permitted in such cases |

| State code / PIN mismatch | System validation may reject the transaction |

Use of “URP” where consignee is unregistered

Where the consignee is not registered under GST or GSTIN is not applicable in the transaction, the value “URP” may be entered in the Ship-To GSTIN field.

This is important for businesses dealing with:

- unregistered buyers;

- project-site deliveries;

- direct delivery to end customers;

- export-related transactions where domestic Ship-To GSTIN may not apply;

- certain delivery scenarios where GSTIN is not available.

However, “URP” should not be used casually. Businesses should maintain proper documentation to justify why GSTIN was not available or not applicable.

Voluntary E-Way Bill closure facility

GSTN has also introduced a new voluntary facility to close an E-Way Bill after delivery of goods is completed.

This facility is not mandatory at present, but it is a significant compliance improvement. It helps create a system record that the goods movement has been completed.

The E-Way Bill may be closed by:

- supplier;

- recipient;

- transporter involved in the transaction;

- driver or authorised person whose mobile number has been provided for closure.

The closure may be done E-Way Bill-wise or date-wise.

Why voluntary E-Way Bill closure is important

At present, many E-Way Bills remain active until expiry of validity even after the goods are delivered. This can create avoidable risk, especially where old or active E-Way Bills are misused.

The voluntary closure facility may help in:

- confirming completion of goods movement;

- improving reconciliation between invoice, E-Way Bill and actual delivery;

- reducing misuse of active E-Way Bills;

- improving internal control over logistics;

- assisting audit trails and GST compliance review;

- reducing future disputes during GST scrutiny or inspection.

For businesses dealing with frequent goods movement, this feature may become a good internal compliance control.

Impact on e-Invoice and IRN-based E-Way Bill generation

The update is not limited to manual E-Way Bill generation. It also affects API-based and IRN-based flows.

The changes apply where:

- IRN and E-Way Bill are generated together;

- E-Way Bill is generated later using IRN;

- Ship-To details are provided in the e-Invoice schema;

- the transaction involves Bill-To/Ship-To or combination scenarios;

- ERP/API integration is used for E-Way Bill generation.

Where Ship-To legal name and Ship-To address are provided and E-Way Bill generation is required, Ship-To GSTIN will also be required. If GSTIN is not available, “URP” may be entered, wherever applicable.

Key validations expected in the system

GSTN has indicated that validations may apply for:

- mandatory Ship-To GSTIN where Ship-To details are provided;

- valid GSTIN;

- Bill-To GSTIN and Ship-To GSTIN not being the same in Bill-To/Ship-To cases;

- Ship-To State Code matching the GSTIN State Code;

- Ship-To PIN Code matching the State Code;

- mandatory GSTIN field in E-Way Bill by IRN API.

These validations mean businesses should not treat this as a mere data-entry change. It requires proper master-data correction and ERP readiness.

What businesses should do before 1 August 2026

Businesses should use the deferred timeline to complete the following actions:

1. Update customer and consignee master data

Customer master, delivery address master, warehouse master, branch master and project-site details should be reviewed.

2. Verify GSTIN of Ship-To parties

Where goods are frequently delivered to third parties, branches, depots, job workers or project sites, their GSTIN status should be verified.

3. Create URP logic for unregistered consignees

ERP systems should allow “URP” in genuine unregistered consignee cases and maintain a proper audit trail.

4. Update ERP and API systems

Businesses using API-based E-Way Bill generation or e-Invoice integration should coordinate with ERP vendors, GSPs and ASPs for sandbox testing.

5. Train billing and dispatch teams

Sales, billing, dispatch, logistics and warehouse teams must understand the difference between Bill-To, Ship-To, Dispatch-From and actual consignee.

6. Review transporter coordination

Transporters and drivers may be involved in voluntary E-Way Bill closure. Businesses should define who will close the E-Way Bill and when.

7. Create internal SOP

A standard operating procedure should be prepared for:

- Ship-To GSTIN reporting;

- URP use;

- E-Way Bill closure;

- post-delivery confirmation;

- exception handling;

- record keeping.

Practical example

A Delhi company sells goods to a registered buyer in Mumbai, but the buyer instructs delivery to its warehouse in Gujarat.

In this case:

- Invoice may be issued to Mumbai GSTIN.

- Goods may be shipped to Gujarat warehouse.

- The E-Way Bill must correctly capture Ship-To details.

- If the Gujarat warehouse has a GSTIN, that GSTIN should be reported.

- If the consignee is unregistered or GSTIN is not applicable, “URP” may be used, wherever applicable.

Wrong reporting may lead to system rejection, mismatch, detention risk or future GST scrutiny.

Common mistakes to avoid

Businesses should avoid the following mistakes:

- entering Bill-To GSTIN again in Ship-To GSTIN field;

- using “URP” despite availability of valid GSTIN;

- failing to update customer delivery locations;

- ignoring e-Invoice and IRN-based E-Way Bill API changes;

- not testing ERP integration before 1 August 2026;

- not training dispatch and logistics teams;

- not defining responsibility for E-Way Bill closure;

- treating voluntary closure as unnecessary without assessing internal control benefits.

Compliance impact for taxpayers

This update is part of GSTN’s larger move towards system-driven compliance and better data matching. E-Way Bill, e-Invoice, GSTR-1, GSTR-3B, GSTR-2B and logistics data are becoming increasingly interconnected.

Therefore, incorrect E-Way Bill reporting may not remain only a transport-document issue. It may also affect:

- GST scrutiny;

- input tax credit reconciliation;

- invoice matching;

- detention proceedings;

- audit trail;

- customer/vendor reconciliation;

- internal compliance rating.

Businesses should therefore review this update seriously.

Professional assistance

Businesses facing difficulty in updating GST systems, E-Way Bill processes, e-Invoice integration or GST compliance SOPs may consider professional support for GST registration and return filing, GST notice and demand defence, GST consultant in Dwarka, CA in Dwarka, and schedule consultation.

Conclusion

The deferment of GSTN’s E-Way Bill enhancements to 1 August 2026 gives businesses additional time, but it should not be treated as a postponement of compliance planning.

The mandatory Ship-To GSTIN requirement and voluntary E-Way Bill closure facility are important steps towards better traceability of goods movement and improved GST data integrity.

Businesses should immediately review their ERP systems, customer master data, consignee records, logistics SOPs and E-Way Bill controls to ensure smooth compliance from 1 August 2026.

GSTN E-Way Bill update 2026, Ship-To GSTIN mandatory, E-Way Bill closure facility, Bill-To Ship-To GST, URP in E-Way Bill, GST E-Way Bill changes 2026, E-Way Bill from 1 August 2026

Leave a Reply