1. Tax on Gift of a Car to a Non-Relative — Clarified

In India, gifts often symbolize goodwill and affection. Yet, the Income-tax Act, 1961 draws a fine line between personal generosity and taxable income. Section 56(2)(x) governs the taxation of gifts received without consideration by an individual or a Hindu Undivided Family (HUF).

While many taxpayers assume all high-value gifts are taxable, the law taxes only certain kinds of “movable properties.” Interestingly, a motor car does not fall within that taxable category — even when gifted by a non-relative.

2. The Governing Provision: Section 56(2)(x)

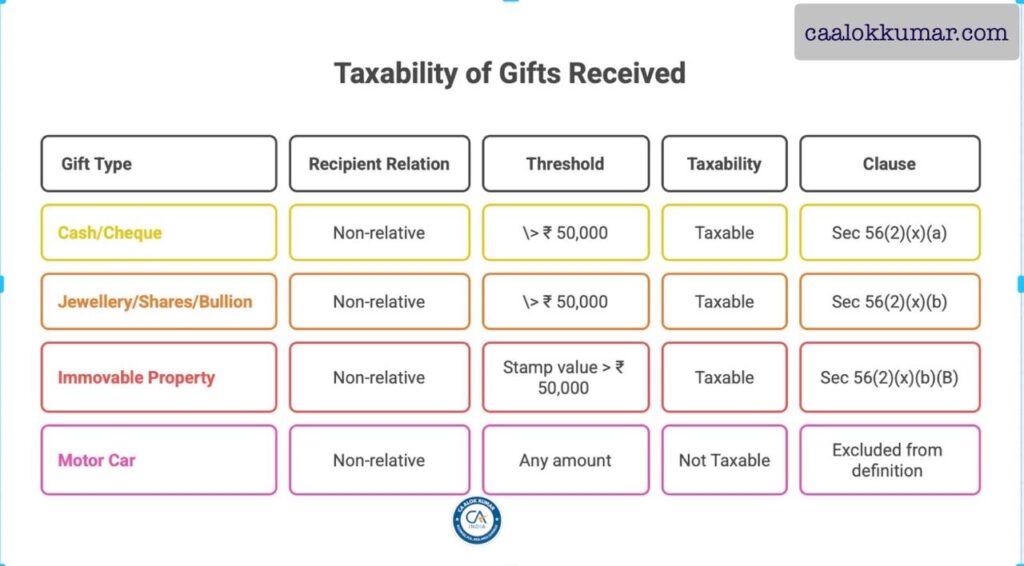

Section 56(2)(x) taxes the fair-market value (FMV) of any “prescribed movable property” received without consideration if its total value exceeds ₹ 50,000 in a financial year.

The section defines “prescribed movable property” as follows:

Shares and securities, jewellery, archaeological collections, drawings, paintings, sculptures, any work of art, bullion, and Virtual Digital Assets (VDAs).

Any movable item outside this definition — for example, furniture, television, or a car — is not treated as “property”for the purpose of this clause

3. Why a Gifted Car Is Not Taxable

According to the official Income Tax Department tutorial (as amended by the Finance Act, 2025):

“Motor car is not covered in the definition of prescribed movable property. Hence, nothing will be charged to tax in case of gift of motor car received by an individual from his friends even though the fair market value exceeds ₹ 50,000.”

This official statement from the Department itself confirms that:

- The recipient (donee) of a car gift owes no income tax on its value; and

- The donor (giver) likewise incurs no gift tax, as India abolished gift tax in 1998.

4. Practical Example

Mr. Chadha receives a car worth ₹ 25 lakh from his friend as a gift.

- The car is a movable asset but not a “prescribed movable property.”

- Hence, Section 56(2)(x) does not apply.

- The gift is fully exempt in the hands of Mr. Chadha, even though it is from a non-relative and its value exceeds ₹ 50,000.

If, however, Mr. Chadha’s friend had transferred ₹ 25 lakh in cash or by cheque for him to purchase a car, the amount would be taxable as a monetary gift, because money is expressly covered under Section 56(2)(x).

5. Documentation and Compliance

To avoid future disputes or scrutiny under the Benami or anti-money-laundering provisions, it is advisable to:

- Execute a simple Gift Deed on stamp paper stating that the transfer is without consideration.

- Register ownership in the donee’s name with the Regional Transport Office (RTO).

- Update insurance and RC to reflect the change of ownership.

- Retain bank and transfer records if the gift involved any payment of road tax or insurance premium.

6. Judicial and Administrative Consistency

No court or tribunal has held a car gift taxable under Section 56. The illustrations in the CBDT’s official publication themselves clarify that a motor car is outside the taxable scope of “prescribed movable property”.

Hence, the Department’s own interpretation — supported by the Finance Act’s language — governs until Parliament amends the definition.

7. Summary Table – Tax on Gift of Car

8. Conclusion

Under present Indian tax law, a gift of a motor car from a friend or non-relative — regardless of its value — is not taxable because a car is not among the “prescribed movable properties” covered by Section 56(2)(x).

However, gifts of money or of assets like jewellery or shares remain taxable when received from non-relatives beyond ₹ 50,000 in a year.

Thus, if you receive a car as a token of friendship, you can accept it without any tax burden — but if the same generosity comes in the form of a bank transfer, be ready to pay income tax.

Official Reference:

Central Board of Direct Taxes (CBDT), “Tax Treatment of Gifts Received by an Individual or HUF — As amended by the Finance Act, 2025,” available on incometaxindia.gov.in

Leave a Reply