ITAT Favors Aishwarya Rai Bachchan in ₹4.11 Crore Section 14A Tax Dispute

Background of the Case (AY 2022–23)

The Mumbai Bench of the Income Tax Appellate Tribunal (ITAT)

For the Assessment Year 2022–23, Aishwarya Rai Bachchan filed returns disclosing around ₹39.3 crore of income. She had earned some tax-free income (exempt from tax) and voluntarily disallowed ₹49 lakh in her return, acknowledging that amount as expenses related to that exempt income (a “suo motu” disallowance). However, the Assessing Officer (AO) was not satisfied. The AO invoked Section 14A of the Income Tax Act (with Rule 8D of the Income Tax Rules) to compute a much higher disallowance. He calculated about ₹4.60 crore of expenses to disallow by applying a flat 1% rate on her investments, and after subtracting the ₹49 lakh she already disallowed, proposed an additional ₹4.11 crore be disallowed. This was striking because her total expenses for the year were only about ₹2.48 crore in reality. In essence, the tax officer’s formulaic approach led to a disallowance far exceeding what she actually spent, prompting a legal dispute that went to the Income Tax Appellate Tribunal (ITAT).

Section 14A and Rule 8D – Explained in Plain Terms

Section 14A of the Income Tax Act, 1961 is a provision designed to prevent taxpayers from deducting expenses that are incurred to earn exempt income (income that isn’t taxable). In simple terms, if you have income on which you don’t pay tax (for example, tax-free bond interest or certain dividends), you cannot deduct the related expenses from your taxable income. The logic is straightforward: since the income itself isn’t taxed, any costs spent to earn that income shouldn’t reduce your taxable profits. This section was introduced to curb the practice of claiming deductions for expenses against income that doesn’t contribute to tax revenues.

Because it’s not always easy to figure out how much expense is incurred “in relation to” exempt income, Rule 8D of the Income Tax Rules provides a standard method to calculate such disallowable expenses. In essence, Rule 8D allows the tax officer to allocate a reasonable portion of a taxpayer’s total expenses as related to exempt income, if the taxpayer’s own calculation is unsatisfactory. The rule typically involves:

- Direct expenses: Any specific expenses clearly incurred to earn exempt income (for example, an investment advisory fee for managing tax-free bond portfolios).

- Interest cost allocation: A proportion of overall interest expense, if the taxpayer has borrowed funds that could be financing investments yielding exempt income. This is usually based on the ratio of investments (that generate exempt income) to total assets.

- Administrative/overhead proxy: A flat percentage of the average value of investments that produce tax-free income, to account for general administrative expenses (for instance, management and maintenance costs). Historically this rate is 0.5% per Rule 8D(2)(iii), though in this case the AO used 1% which doubled the effect.

Importantly, Rule 8D is not applied automatically. The tax officer must first examine the taxpayer’s accounts and explanation. If the officer finds that the taxpayer’s own disallowance (or claim of having no related expense) is not correct or adequate, and records reasons for this dissatisfaction, only then can the Rule 8D formula be invoked. In other words, the law requires a recorded justification – the officer can’t arbitrarily pick a formulaic disallowance without showing why the assessee’s calculation is unsound. This safeguard was central to Aishwarya Rai’s case.

The AO’s Rationale: Applying Section 14A Mechanically

In Aishwarya’s scrutiny assessment, the Assessing Officer rejected her ₹49 lakh self-disallowance as too low. The AO noted that she had made large investments and earned substantial exempt income (around ₹2.15 crore of tax-free interest/dividends in that year). The officer’s rationale was that interest-free funds were used to earn exempt income, and therefore a higher proportion of expense needed to be disallowed under Section 14A. Without pinpointing specific expenses that she missed, the AO resorted to Rule 8D’s presumptive formula.

Using a 1% of average investments approach, the AO calculated about ₹4.60 crore as the total expenditure allocable to exempt income. Since Aishwarya had already disallowed ₹49.08 lakh herself, the AO added an extra ₹4.11 crore on top of her computation. Essentially, the tax officer believed her actual expenses didn’t matter – a fixed percentage of her investments was disallowed as a matter of course. This “broad-brush” method ignored the fact that her entire actual expenditure that year was only ~₹2.48 crore. The disallowance was therefore not only significantly higher than her own calculation, but even higher than all the expenses she actually incurred in the year, which raised concerns of overreach.

The AO also did not explicitly document why he thought her ₹49 lakh allocation was insufficient beyond citing the Section 14A/Rule 8D mandate. There was no specific finding of any particular expense that was improperly claimed. This lack of a reasoned basis and the evidently excessive figure set the stage for appeal.

CIT(A)’s Findings: Partial Relief for the Taxpayer

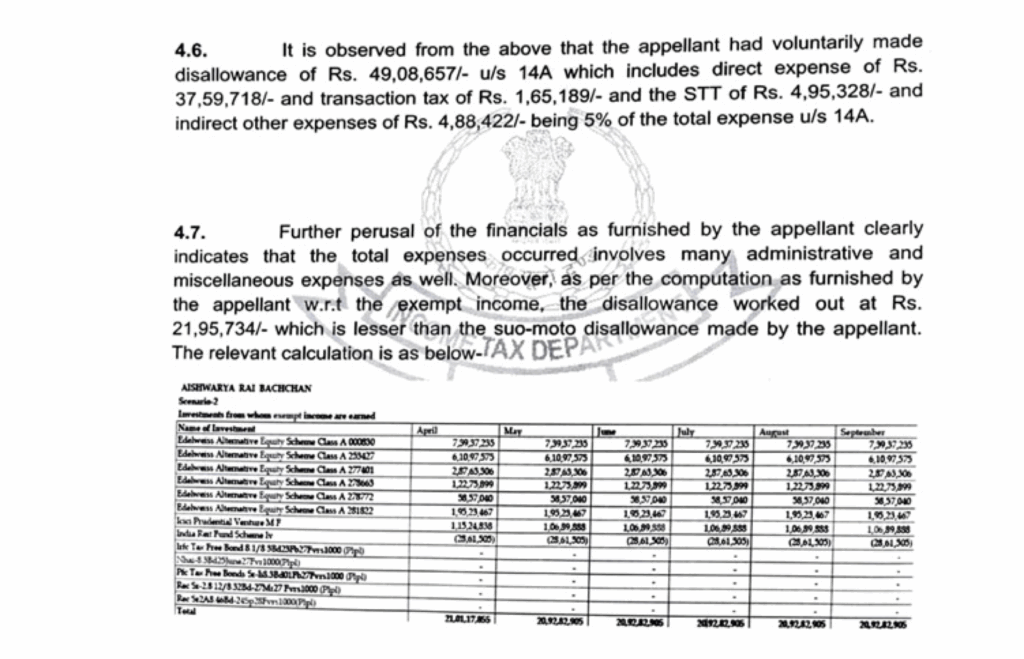

On appeal, the Commissioner of Income Tax (Appeals) – a senior appellate authority – examined the issue. The CIT(A) noted that Aishwarya’s total expenses were around ₹2.48 crore, a figure far below the AO’s computed disallowance. The CIT(A) found the AO’s use of 1% of investments “without demonstrating the link” between those funds and any actual expense to be flawed. In simpler terms, the AO had not shown any actual expenditure that warranted disallowing beyond what the taxpayer already did.

The CIT(A) observed that Rule 8D is meant to estimate expenses only when necessary, not to inflate disallowances beyond reality. Applying a flat rate in this case was deemed unreasonable and not backed by facts. Importantly, the CIT(A) highlighted the legal requirement that the AO must record satisfaction (with reasons) if rejecting the taxpayer’s computation – which was not done here. In support, the CIT(A) even referenced the Supreme Court’s ruling in Maxopp Investment Ltd. v. CIT (2018), a case which underscored that the tax officer must objectively scrutinize the assessee’s calculation before making a higher disallowance.

As a result, the CIT(A) deleted the ₹4.11 crore additional disallowance, effectively accepting that Aishwarya’s suo motu ₹49 lakh disallowance was sufficient. This outcome meant that only the amount the actress herself had disallowed would stand, and nothing further, since the Revenue had not justified any higher figure. Unsurprisingly, the Income Tax Department (the Revenue) was dissatisfied with this decision and appealed to the ITAT, arguing that the CIT(A) had wrongly favored the taxpayer.

ITAT Ruling: No Disallowance Beyond Actual Expenditure

The Mumbai Bench of the Income Tax Appellate Tribunal (ITAT) analyzed the case and ultimately upheld the CIT(A)’s decision in Aishwarya Rai Bachchan’s favor. The ITAT dismissed the Revenue’s appeal, reinforcing some key principles:

- Lack of AO’s “Satisfaction”: The tribunal noted that the AO failed to record a clear reason for why the ₹49 lakh already disallowed by Aishwarya was inadequate. This procedural step is mandatory under Section 14A(2)/(3). Simply invoking Rule 8D without explaining the necessity renders the disallowance invalid. The ITAT echoed that unless the AO can show how the taxpayer’s calculation is wrong, the taxpayer’s figure should be accepted by default.

- Disallowance Cannot Exceed Actual Expenses: It struck the Tribunal as illogical that the computed disallowance (₹4.60 crore total) far exceeded the actual expenditure (₹2.48 crore) incurred by the assessee. Disallowing more expense than was actually paid or booked in the accounts is “devoid of any logic and clearly unreasonable,” the ITAT observed. In other words, Rule 8D cannot be used to conjure a fictional expense amount – it is meant to apportion real expenses, not inflate them. The tribunal firmly stated that no disallowance under Section 14A/Rule 8D should ever exceed the actual expenditure claimed.

- Investments with No Exempt Yield to be Excluded: The ITAT also pointed out that the AO shouldn’t have included investments that did not actually produce any tax-free income in that year** when calculating the disallowance. This is a subtle but important aspect – if certain holdings yielded no dividend or exempt return in the relevant period, allocating expenses to them under Section 14A is questionable. The disallowance is meant to correlate to earning exempt income; idle or non-income-generating investments shouldn’t inflate the calculation.

- AO’s Mechanical Approach Rejected: Overall, the Tribunal found that the AO took a mechanical, “one-size-fits-all” approach by applying 1% across the board, without examining the actual accounts and submissions of the taxpayer. Aishwarya’s counsel had given detailed replies during assessment, explaining that very minimal expenses were linked to her tax-free earnings, but the AO ignored these arguments. The ITAT regarded this as a failure on the AO’s part to engage with the facts. Since the AO “had not articulated any reasoned basis” to doubt the assessee’s computation and the proposed addition was disproportionate, the ITAT confirmed that the additional ₹4.11 crore disallowance lacked any merit.

By ruling in her favor, the ITAT deleted the entire ₹4.11 crore addition and confirmed that her original self-disallowed ₹49 lakh was appropriate. In summary, Aishwarya Rai Bachchan’s appeal prevailed because the tax department could not justify a larger disallowance either in law or on facts.

Judicial Principles Reinforced (Maxopp, Godrej & Boyce, etc.)

This case highlights and reinforces broader judicial principles governing Section 14A, as established in landmark rulings like Maxopp Investment Ltd. (SC, 2018) and Godrej & Boyce Mfg. Co. (Bombay HC & SC). Firstly, the tax officer must apply Section 14A with care and not by rote. The “recorded satisfaction” requirement is not a mere technicality – it ensures the AO actually identifies why a taxpayer’s own disallowance is too low. The Supreme Court in Maxopp underscored that the process under Section 14A istriggered only if the AO is not satisfied with the assessee’s calculation and documents that fact**, preventing arbitrary or excessive claims by the Revenue. In Aishwarya’s case, this principle was clearly in play: the absence of a cogent reason by the AO undermined the additional disallowance.

Secondly, courts have consistently held that Section 14A disallowances should bear a relationship toactual expenditure incurred to earn exempt income. The Godrej & Boyce jurisprudence, for instance, emphasized that conjectural or excess disallowances – especially those disconnected from real outlays – are impermissible. The ITAT’s comment that a ₹4.60 crore disallowance against ₹2.48 crore of expenses was “devoid of logic” is a practical affirmation of this rule. In fact, some high courts (e.g. in Joint Investments Pvt. Ltd. and other cases) have gone further to say that disallowance under Section 14A should not exceed the exempt income** earned in that year – reinforcing that it’s not meant to punish taxpayers with an overkill formula.

Finally, the ruling touches on the idea that only investments yielding exempt income should factor into the disallowance computation. This aligns with a commonsense principle: if an asset didn’t produce any tax-free income, then expenses associated with it (if any) shouldn’t be disallowed under Section 14A for that year. While the law on that specific point has seen differing views, the ITAT’s stance here adds to the pro-taxpayer perspective that the scope of Section 14A is confined to the actual scenario of earning exempt income, not just having investments.

In short, the outcome of this case resonates with the higher court doctrines – don’t overshoot the actual expense, follow the section’s conditions strictly, and keep the calculation reasonable and rooted in facts.

Similar High-Profile and Bollywood Celebrity Tax Disputes for Context

Aishwarya’s victory is one in a line of high-profile tax cases where Bollywood celebrities have contested aggressive tax adjustments. For instance, Amitabh Bachchan faced a well-known tax dispute years ago regarding his income from the show Kaun Banega Crorepati (KBC). In that case, he had initially claimed certain expenses and later withdrew that claim, which led to a legal tussle. The Supreme Court eventually intervened, allowing the tax department to re-examine his assessments on the reasoning that large expense claims (followed by withdrawal) warranted proper scrutiny in the interest of the Revenue. That episode underscored that even legendary actors are not beyond the reach of Section 14A-like issues: if substantial tax-free receipts or expense claims are involved, authorities will closely investigate whether any disallowance is needed. In Mr. Bachchan’s case, while the facts differed from Aishwarya’s, the underlying theme was similar – the tax officer must not overlook potential disallowable expenses, and conversely, cannot conjure disallowances without basis.

Similarly, Shah Rukh Khan recently had a significant win in a tax matter. In a dispute over his income from the film ’Ra.One’ (Assessment Year 2012–13), the ITAT ruled in SRK’s favor and quashed a reassessment order by the tax department. The tax authorities had attempted to deny him certain claims (in his case, foreign tax credits and related deductions), but the tribunal found that the department acted beyond permitted time limits and without fresh evidence. While this case revolved around reassessment and foreign tax credit rather than Section 14A, it highlights a common thread: Bollywood stars often find themselves defending the correctness of their tax filings and claims, and the appellate tribunals/courts frequently have to ensure that tax law is applied fairly rather than punitively. Other celebrities like Salman Khan, Deepika Padukone, and Priyanka Chopra have also reportedly been subject to tax inquiries or adjustments in the past (ranging from undeclared incomes to disallowances of expenses), indicating that the tax department keeps a close watch on high earners. The key takeaway is that the principles of law – such as proper procedure and evidence – apply equally to celebrities and common taxpayers. High-profile cases tend to shine a spotlight on these principles, as seen in the Bachchan and Khan cases, reinforcing them for everyone.

Broader Implications for Taxpayers and Practitioners

The ITAT’s ruling in Aishwarya Rai Bachchan’s case carries important implications for taxpayers and tax practitioners dealing with Section 14A disputes:

- Substance Over Formula: The decision makes it clear that tax officers cannot blindly rely on Rule 8D formulas to jack up disallowances. Any disallowance must be grounded in the taxpayer’s actual expense pattern. If a computed number overshoots reality, it won’t hold up on appeal. Practitioners should therefore document actual expenditures and their nexus (or lack thereof) to exempt income, to counter unreasonably high disallowances.

- AO’s Mandatory Duty of Explanation: Taxpayers should note that if they have already made a reasonable suo motu disallowance, the AO must give a cogent reason to disagree with it. This ruling reinforces that any Section 14A adjustment requires a recorded satisfaction note by the AO. In practice, if an assessing officer adds a disallowance without explicitly addressing the taxpayer’s own calculation, that addition is vulnerable to challenge. Advisors can cite this case to insist on transparency and reasoning in assessment orders.

- Ceiling on Disallowances: The outcome affirms an intuitive cap: the disallowance under Section 14A cannot exceed the actual expenditure claimed in the accounts. It also hints at the principle (supported by other rulings) that the disallowance should ideally not exceed the exempt income earned. This puts a natural check on overzealous computations. Tax professionals can leverage this point – if an AO’s calculation overshoots either the expense or the exempt income, it’s a strong ground for appeal.

- Selective Investment Consideration: The tribunal’s comment about excluding investments that didn’t yield exempt income in the year is a reminder to officers and taxpayers alike to be nuanced. Practitioners should argue to remove such investments from the Rule 8D base; conversely, taxpayers should be prepared with details of income-yielding vs non-yielding investments to make this argument.

- Reaffirming Fairness in Tax Administration: At a higher level, this ruling (and others like it) reassures that appellate bodies will step in to correct unfair or unfounded additions. It encourages taxpayers to appeal unreasonable Section 14A adjustments, knowing that tribunals and courts consistently uphold the principle that only genuine expenditure attributable to exempt income should be disallowed – nothing more, nothing less.

In conclusion, the ITAT’s judgment in favor of Aishwarya Rai Bachchan not only resolves her individual case but also strengthens the precedent for equitable application of Section 14A. It serves as a caution to tax authorities against excessive disallowances and provides taxpayers and their advisors with authoritative support to ensure that tax-free income adjustments are made judiciously. This case will likely be cited in future disputes to emphasize that tax law is about reasonable estimations grounded in reality, not aggressive overreach, thereby contributing to a more balanced resolution of Section 14A controversies moving forward.

Leave a Reply