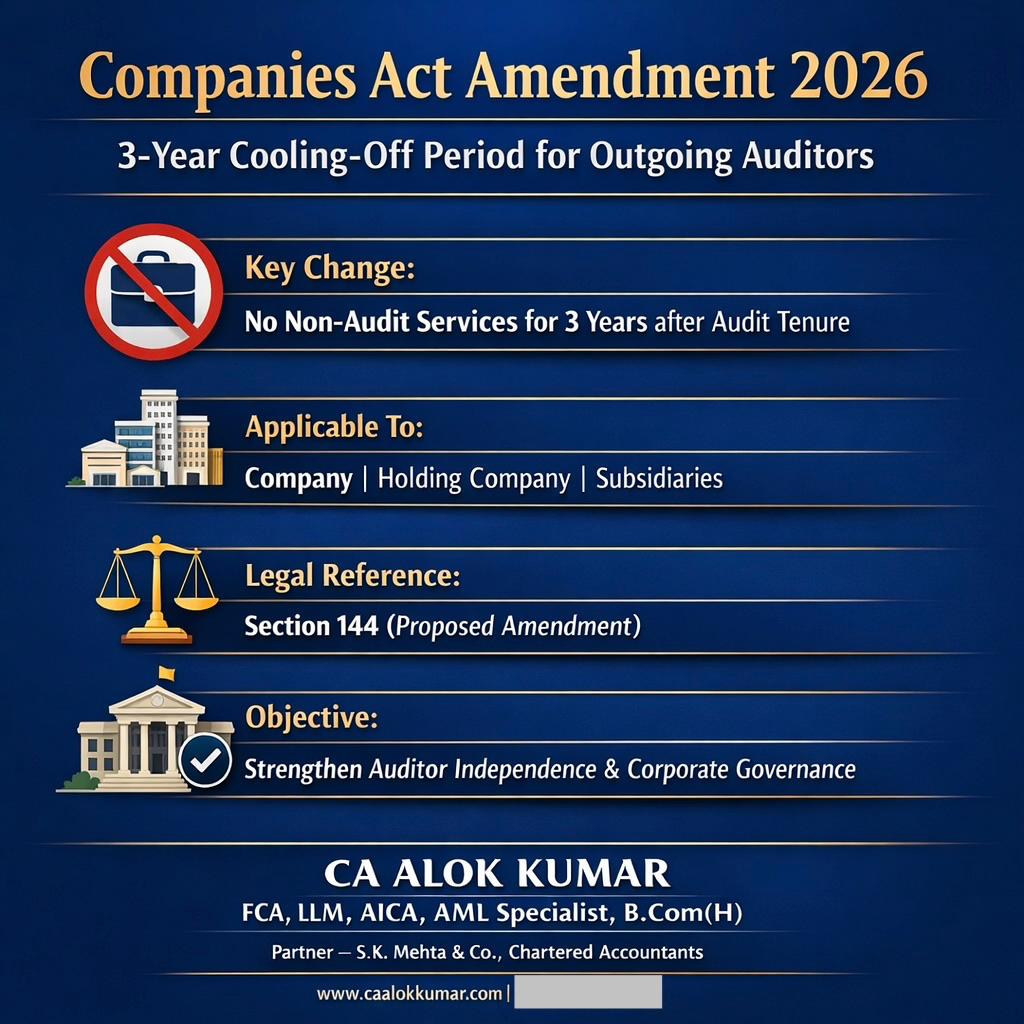

Outgoing Auditors Barred from Non-Audit Services for 3 Years: A Major Companies Act Amendment Explained

📢 Introduction

In a significant step towards strengthening corporate governance, auditor independence, and financial transparency, the Government of India has proposed a crucial amendment to the Companies Act, 2013.

Under this amendment, outgoing auditors will be restricted from providing non-audit services to the same company for a period of 3 years after completion of their tenure.

This move is expected to have a major impact on Chartered Accountants, audit firms, and companies, particularly in ensuring independence and eliminating conflicts of interest.

🔍 Legal Background – Sections Involved

The proposed amendment is linked with the following key provisions:

- Section 144 – Restriction on auditors from rendering certain services

- Section 139(2) – Mandatory rotation of auditors

👉 As per Section 139(2), certain classes of companies must rotate auditors after a fixed tenure to prevent familiarity threats and ensure independence.

👉 Section 144 already prohibits auditors from providing specified non-audit services during their tenure.

⚖️ What is the Proposed Amendment?

The amendment proposes insertion of a new proviso under Section 144, which provides that:

- After completion of tenure (including rotation),

- The auditor or audit firm shall not provide any non-audit services to:

- The same company

- Its holding company

- Its subsidiary companies

- For a period of 3 years (cooling-off period)

🔄 Earlier Law vs New Amendment

| Particulars | Earlier Position | After Amendment |

| Restriction period | Only during audit tenure | During tenure + 3 years after tenure |

| Non-audit services | Allowed post resignation/rotation | Completely restricted for 3 years |

| Objective | Prevent conflict during audit | Prevent post-audit influence and conflict of interest |

🎯 Objective of the Amendment

The primary objectives behind this amendment are:

✔️ Strengthening Auditor Independence

Ensures auditors remain unbiased even after completion of their tenure.

✔️ Eliminating Conflict of Interest

Prevents auditors from auditing accounts and then immediately advising the same client.

✔️ Improving Financial Reporting Credibility

Enhances trust of stakeholders, investors, and regulators.

✔️ Aligning with Global Best Practices

Similar cooling-off norms exist in many international jurisdictions.

⚠️ Practical Impact on Stakeholders

🔹 Impact on Companies

- Need to appoint separate firms for advisory and consultancy services

- Audit Committee must ensure strict independence compliance

- Increased focus on vendor segregation

🔹 Impact on Chartered Accountants & Audit Firms

- Loss of immediate consulting assignments post audit tenure

- Need to restructure service offerings and client relationships

- Greater emphasis on ethical compliance and independence

🔹 Impact on Corporate Governance

- Reduces risk of biased reporting

- Improves transparency and accountability

- Strengthens investor confidence

🧾 Link with Auditor Rotation

Under Section 139(2):

- Individual auditor → Maximum 5 years

- Audit firm → Maximum 10 years

- Cooling-off period already exists for reappointment

👉 The new amendment extends the concept of cooling-off to non-audit services, making the framework more robust.

📌 Why This Amendment is Important

This amendment closes a major loophole where:

➡️ Auditors could audit a company and immediately start consultancy work

➡️ This created a risk of compromised independence and biased audit opinions

Now, with a 3-year restriction, such practices will be significantly curtailed.

The proposed amendment seeks to address this gap by introducing a mandatory cooling-off period of three years, during which the outgoing auditor or audit firm is prohibited from providing any non-audit services to the same company, its holding company, or its subsidiary entities. This restriction applies irrespective of the nature of services and aims to create a clear separation between audit and advisory roles, thereby reinforcing the principle that audit independence must extend beyond the period of engagement.

From a governance perspective, this amendment is a progressive step towards enhancing the integrity of financial reporting systems in India. Auditors play a fundamental role in validating the accuracy and fairness of financial statements, and their independence is essential for maintaining stakeholder confidence. The introduction of a cooling-off period ensures that auditors do not develop economic dependencies or future expectations that could compromise their professional judgment.

The impact of this amendment is expected to be far-reaching across the corporate and professional ecosystem. Companies will be required to adopt a more structured and compliant approach in engaging professional firms, ensuring that audit and consultancy services are clearly segregated. Audit Committees, in particular, will need to strengthen oversight mechanisms to ensure compliance with the revised provisions of Section 144 and to avoid any potential violations.

For Chartered Accountants and audit firms, this amendment necessitates a strategic realignment of service offerings. The traditional model of transitioning from statutory audit to advisory services for the same client will no longer be feasible within the restricted period. Firms will need to re-evaluate their client engagement strategies, build independent advisory verticals, and ensure strict adherence to ethical standards prescribed under the Companies Act and ICAI Code of Ethics.

This reform also aligns India with global best practices in audit regulation, where cooling-off periods and restrictions on non-audit services are considered essential safeguards against conflicts of interest, self-review threats, and undue influence. By extending the restriction beyond the audit tenure, the amendment reinforces the concept that independence is not merely procedural but substantive in nature.

In practical terms, the amendment is expected to enhance transparency, improve audit quality, and strengthen investor confidence in financial disclosures. It also reflects the increasing emphasis of regulators on accountability, governance standards, and ethical conduct in professional services. The move is particularly relevant in the current environment, where regulatory scrutiny over financial reporting and audit practices has intensified.

In conclusion, the proposed restriction on outgoing auditors from providing non-audit services for a period of three years represents a landmark reform in India’s corporate regulatory framework. It effectively closes a critical loophole, ensures continuity of auditor independence, and promotes a more robust and transparent financial reporting ecosystem. For companies, audit firms, and professionals, this amendment underscores the need for enhanced compliance, ethical discipline, and a clear demarcation between audit and advisory functions.

Companies Act amendment 2025, Section 144 of Companies Act amendment India, auditor independence India, audit rotation rules India, non-audit services restriction, MCA update auditors, cooling-off period auditors India, corporate governance India, ITR Filing Near Me, audit compliance Companies Act, CA practice restrictions India, CA in Dwarka Delhi, Tax Consultant in Delhi, audit firm regulations India, MCA Company Audit in India

Leave a Reply