Supreme Court Form 15CB Judgment – CA Liability Under PMLA Clarified

Introduction

The Supreme Court of India has recently delivered a significant judgment clarifying the liability of Chartered Accountants (CAs) under anti-money laundering laws for merely issuing Form 15CB certificates. In Deputy Director v. K. Murali Krishna Chakrala (SLP (Crl) Diary No. 8123/2024), the Court affirmed that a CA’s bona fide issuance of Form 15CB (the tax certificate for foreign remittances) does not itself amount to “assisting” in money laundering. This ruling provides much-needed relief to the CA profession and clear guidance on money laundering compliance in India. It draws on key legal provisions – Section 195(6) of the Income-tax Act, Rule 37BB of the Income-tax Rules, and Section 3 of the Prevention of Money Laundering Act (PMLA) – to delineate the boundary between professional duty and criminal complicity. The outcome has important implications for CA liability under PMLA, reinforcing that professional certification in due course of law criminal conspiracy, and offers lessons in Chartered Accountant risk management.

Case Background: Bogus Imports, Form 15CB & Alleged Money Laundering

The case arose from an Enforcement Directorate (ED) prosecution against K. Murali Krishna Chakrala, a practicing CA, who had issued five Form 15CB certificates for a Chennai-based company B.K. Electro Tool Products. These certificates were for outward remittances in relation to import payments, as required under tax law. Unbeknownst to the CA, the import transactions were allegedly bogus. An investigation revealed that about ₹8 crore was remitted abroad through fictitious bank accounts using forged import documents. The ED contended that by certifying these transactions, the CA had facilitated the illegal transfers – effectively accusing him of “knowingly assisting” the laundering of “proceeds of crime” in violation of Section 3 PMLA.

Murali Krishna (the CA) maintained that his role was purely that of a professional providing a tax certification service. He asserted that he issued Form 15CB in good faith, based on the documents and declarations provided by his client, and had no knowledge of any fraud. In fact, all other banks had processed similar remittances without requiring Form 15CB, and he was approached only for one particular bank’s compliance needs. He charged a nominal fee (₹1,000 per certificate) and had no stake in the underlying transactions. Thus, he argued, he was not part of any conspiracy but was being unfairly implicated for simply doing his job. The dispute eventually reached the Madras High Court via a criminal revision petition filed by the CA after his discharge plea was initially rejected by the trial court.

Key Legal Provisions: Section 195(6) IT Act, Rule 37BB & Section 3 PMLA

Understanding the legal context is crucial. Section 195(6) of the Income-tax Act, 1961 imposes an obligation on any person responsible for paying any sum to a non-resident to furnish information about the remittance to the tax authorities. This provision was introduced to monitor foreign payments and ensure tax compliance. Rule 37BB of the Income-tax Rules, 1962 specifies the mechanism: it prescribes the use of Form 15CA (an online declaration by the remitter) and Form 15CB (a certificate from a CA) for certain foreign remittances. In essence, Form 15CB is a tax determination certificate where the CA certifies the nature of the remittance, applicable tax treaty provisions, and that due taxes (TDS) have been accounted for as required. Indian law mandates Form 15CB for payments exceeding ₹5 lakh that are taxable to the non-resident, before the bank can remit the funds abroad. Thus, the CA’s involvement via Form 15CB is a statutory compliance duty under the Income-tax Act and Rules.

On the other hand, Section 3 of the PMLA, 2002 defines the offence of money laundering. In broad terms, a person is guilty of money laundering if they directly or indirectly attempt to indulge or knowingly assist in any process or activity connected with the proceeds of crime (such as concealment, possession, acquisition or use of such proceeds) and project or claim them as untainted property. The ED’s case hinged on this provision – alleging that by issuing the Form 15CB certificates, the CA “knowingly assisted” in the processing of illicit funds, thus becoming part of the money-laundering activity. Crucially, PMLA requires a mental element of knowledge or intent; merely performing a service that is later misused by others does not automatically equate to mens rea for money laundering. This distinction became the fulcrum of the court’s analysis.

Madras High Court Findings (457 ITR 579) – Discharge of the CA

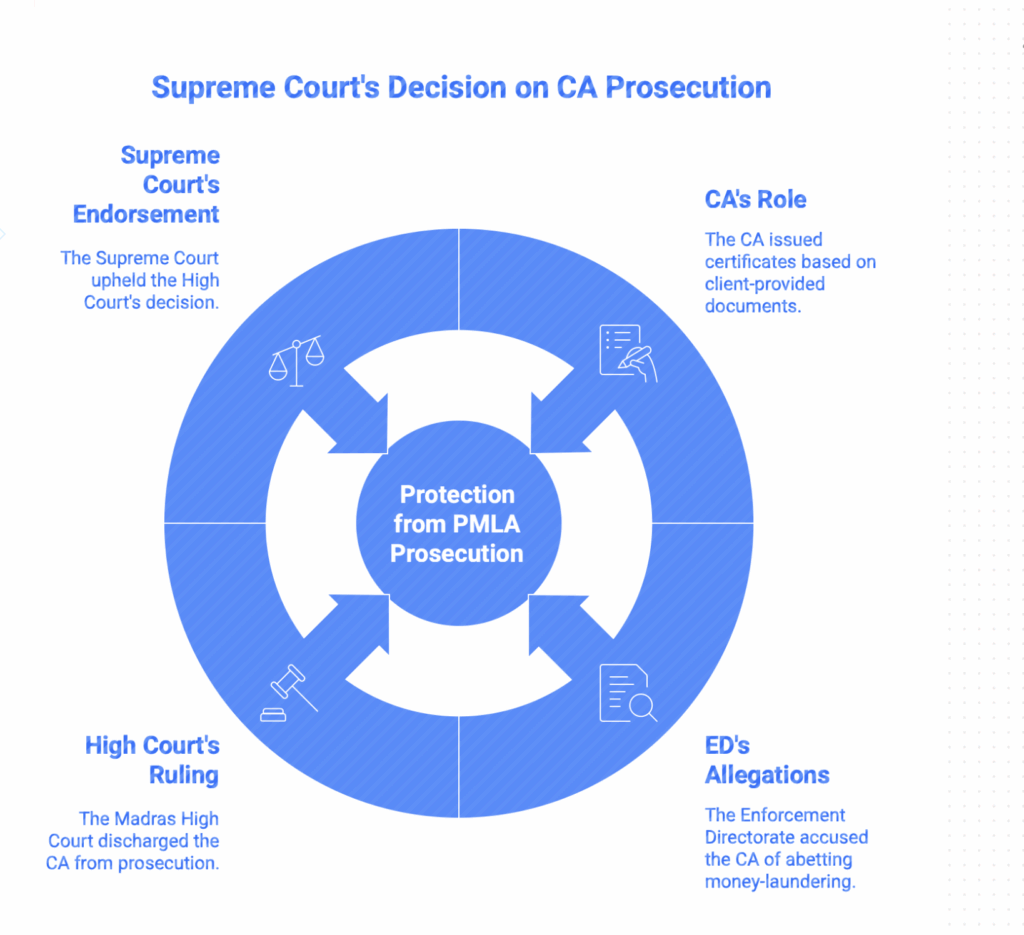

The Madras High Court, in [2023] 457 ITR 579 (Madras), emphatically ruled in the CA’s favor and quashed the prosecution. The Court drew a clear line between professional certification and criminal involvement. Key findings from the High Court (bench of Justice P.N. Prakash and Justice G. Chandrasekharan) include:

- Limited Scope of CA’s Role: Under Rule 37BB and related provisions, a chartered accountant’s role in issuing Form 15CB is confined to verifying the nature of the remittance and the applicable tax provisions (TDS/DTAA) – nothing more. The CA must check, for example, whether the payment is chargeable to tax, the correct rate of TDS, and certify accordingly (as per the documents provided), but is not expected to investigate the genuineness of the underlying transaction documents.

- No Duty to Detect Fraud: The High Court held that a CA “is not required to go into the genuineness or otherwise of the documents submitted by his clients.” In other words, if a client furnishes invoices, bills of entry, contracts etc. to support the remittance, the CA can ordinarily rely on them at face value for tax certification purposes. Unless there are obvious red flags, a CA is not an investigator or auditor of the transaction’s authenticity in a Form 15CB scenario.

- Lack of Mens Rea: Importantly, there was no evidence that Murali Krishna (the CA) had knowledge or intent to assist in any crime. He had no connection to the fake accounts or the end-use of funds; he simply issued certificates in the ordinary course of his practice and received a standard fee. The Court noted that mere issuance of five Form 15CB at a client’s request, by itself, does not drag the CA into a conspiracy to launder money. There was no “knowing assistance” – at least nothing beyond the client’s assertions – therefore the basic ingredient of the PMLA offense was missing.

- Professional vs. Criminal Acts: Drawing an analogy, the High Court likened the CA’s certification to a lawyer rendering a legal opinion – the professional provides a service based on information given, and should not be held criminally liable if the client misuses that service without the professional’s knowledge. In essence, professional duty does not automatically translate to abetment of a client’s crime.

- Discharge and Witness Status: Based on the above reasoning, the High Court discharged the CA from the PMLA prosecution. In fact, recognizing his lack of intent and his cooperation with investigators, the Court observed that he could at best be a prosecution witness in the case against the actual launderers, not an accused. This was a strong message that the enforcement agencies had overreached by charging him.

Thus, the Madras High Court’s judgment established that issuing Form 15CB in good faith, in compliance with Section 195(6)/Rule 37BB requirements, does not amount to “assistance” in money laundering. It was a significant precedent underscoring that CAs cannot be made scapegoats for their clients’ misconduct when they themselves acted without culpable intent.

Supreme Court’s Decision – Affirmation of No Criminal Liability

The Directorate of Enforcement (through the Deputy Director) challenged the High Court’s decision in the Supreme Court, but met with no success. The ED’s Special Leave Petition (SLP (Crl.) Diary No. 8123/2024) was dismissed by the Supreme Court on 18 March 2024, effectively upholding the High Court’s ruling. Subsequently, on 10 November 2025, a Supreme Court bench of Justice Surya Kant and Justice Joymalya Bagchi passed a detailed order reiterating that there was “no valid ground to interfere” with the Madras High Court’s judgment dated 08.08.2024. The Supreme Court thus affirmed the discharge of the CA and terminated all proceedings against him under PMLA.

Quoting the Supreme Court’s order: “…there is no valid ground to interfere with the impugned [Madras HC] order…”. The Court refused to reopen or recall the case, cementing the High Court’s reasoning as final. By dismissing the ED’s appeal, the apex court essentially endorsed the principle that a CA acting bona fide within the scope of Form 15CB certification cannot be held criminally liable under PMLA unless clear evidence of mens rea (knowing assistance in laundering) is shown.

In its analysis, the Supreme Court emphasized two points. First, the boundary of professional liability: compliance certifications like Form 15CB are administrative in nature (to ensure tax laws are followed), not investigative. Certification ≠ Complicity. Merely because a CA’s certificate was used in a transaction that turned out to be illicit does not mean the CA “laundered” money, absent deliberate involvement. Second, the Court highlighted that anti-money laundering enforcement should focus on “genuine offenders, not professionals performing regulated duties”. Dragging compliant professionals into criminal cases without proof of collusion would not only be unjust to individuals but also disrupt the system of compliance where banks and regulators rely on professionals’ certifications.

The upshot of the Supreme Court’s judgment is a clear affirmation: Issuing a Form 15CB in the ordinary course of one’s practice, relying on client-provided information, does not amount to abetment of money laundering. The CA in this case was exonerated, and the ED’s aggressive stance was curtailed. The ruling has since been welcomed as it balances the objectives of PMLA with the practical role of CAs in tax compliance.

Legal Implications for Practicing CAs in India

A conceptual depiction of a Chartered Accountant facing legal peril. The Supreme Court’s judgment shields CAs from unwarranted PMLA charges when they act in good faith, reinforcing that professional duties should not be conflated with criminal intent.

The Supreme Court’s decision has far-reaching implications for practicing Chartered Accountants and other professionals in India:

- Reassurance of Limited Liability: CAs can take comfort that performing their statutory duties (like issuing Form 15CB) in good faith will not by itself make them liable under PMLA. This judgment draws a protective boundary – professional compliance work, without more, is not “money laundering”. It reassures professionals that they will not be hauled up for their clients’ misdeeds so long as they are not consciously complicit. In the Indian context, where fear of draconian laws like PMLA was mounting, this offers relief and clarity.

- Emphasis on Mens Rea: The ruling reiterates the importance of mens rea (guilty mind) in criminal liability. For regulators and investigators, it sends a message that charging a CA (or any professional) under PMLA requires evidence of knowing participation in the laundering process. Merely because a CA’s name appears on a certificate used in a tainted transaction is insufficient. This could temper overzealous enforcement actions and reduce the risk of harassment of professionals in high-profile financial investigations.

- Professional Conduct and Standards: Conversely, CAs are implicitly reminded that willful blindness or collusion would attract liability. The flip side of the judgment is that it does not condone negligent or unethical behavior; it only protects bona fide conduct. If a CA knowingly falsifies a certificate or ignores obvious red flags, they could still face consequences (be it under PMLA, aiding and abetting fraud, or professional misconduct rules). Thus, the case highlights the outer limit of responsibility: CAs must perform due diligence to the extent expected, but they are not expected to be detectives. Staying within that boundary keeps them safe from criminal liability.

- Impact on Compliance Ecosystem: For banks, financial institutions, and regulators, the judgment clarifies the role of CA certificates in compliance. It reinforces that Form 15CB is essentially a tax compliance tool, not a guarantee of transaction bona fides beyond tax matters. Banks should continue to do their own KYC and anti-money laundering checks; they cannot rely solely on a CA’s certificate for genuineness of trade. This multi-layered compliance approach is in line with global money laundering compliance norms, where each stakeholder (remitter, bank, professional) has defined responsibilities.

- Precedent for Other Professions: Although this case specifically involved a CA, its reasoning could apply to other professionals like lawyers, company secretaries, or valuers who issue certificates or opinions in regulatory matters. It underscores a general principle: if a professional adheres to the standards of their role and lacks criminal intent, they should not be criminally liable for clients’ misuse of their work. This is an important precedent in India’s evolving jurisprudence on professional liability and financial crimes.

In summary, the Supreme Court has struck a balance between enforcing anti-money laundering laws and protecting the professional independence of CAs. It has signaled that “Professional certification under fiscal law cannot be criminalized unless there is conscious participation in the wrongdoing”. This delineation is crucial for risk management in the CA community, which can now discharge their duties with more confidence, provided they remain vigilant and honest.

Best Practices for CAs When Issuing Form 15CB

While the judgment provides legal protection for bona fide actions, practicing CAs should continue to follow best practices to mitigate risks and uphold compliance standards:

- Conduct Due Diligence (Within Reason): Always scrutinize the documents provided by the client for Form 15CB – e.g. invoices, import/export contracts, bank details, PAN of the non-resident, etc. Ensure the nature of remittance is clearly understood (e.g. royalty, import of goods, services payment) and check if it matches the supporting documents. While you are not required to authenticate each document’s genuineness, exercising a healthy degree of professional skepticism is wise. If something looks obviously irregular (e.g. mismatch in amounts, suspicious beneficiary jurisdictions, forged-looking papers), seek clarification or additional proof from the client before certifying.

- Document Your Basis: Maintain working papers or notes on how you arrived at the conclusions in Form 15CB. Document the information reviewed – for instance, note that you relied on the client’s invoice #1234 dated X, bill of entry dated Y, and that as per these the payment is for import of machinery attracting no TDS under Section 195, etc. This creates an audit trail of your reasonable steps. In case of any inquiry, such records demonstrate that you did your due diligence in good faith. It’s part of good risk management for Chartered Accountants to have backup for certifications issued.

- Stay Within the Scope: Remember that your certification is about tax and remitment compliance – specifically, confirming whether the payment is taxable and if so, that due tax is deducted or the applicable DTAA provisions are considered. Do not venture beyond this scope in the certificate. Avoid making any declarations that all underlying documents are genuine or that the transaction is bona fide beyond tax law – such assertions are neither required nor advisable. Stick to the language of Form 15CB and applicable rules.

- Use Disclaimers if Necessary: If you harbor any doubts or if certain information couldn’t be independently verified, it’s acceptable to include a note or disclaimer in your working papers (and if possible, in the certificate or cover letter) to the effect that you have relied on information provided by the client. The standard Guidance Note on Reports/Certificates for Special Purposes issued by ICAI permits inclusion of such caveats when appropriate, to make the scope of your work clear. For example, stating that “this certification is based on documents and declarations furnished by the client, and the CA has not audited the source documents for accuracy” can be prudent in certain cases.

- Keep Updated with Regulations: Tax and FEMA regulations on foreign remittances (Forms 15CA/CB, Rule 37BB exemptions, thresholds, etc.) change from time to time. Ensure you are using the latest forms and following the latest instructions from the Income Tax Department. For instance, currently Form 15CB is not needed for certain import remittances up to ₹5 lakh or those covered in the specified Rule 37BB exemption list (like small import payments, travel, education expenses, etc.). Filing forms when not required can create unnecessary exposure, and conversely not filing when required can lead to penalties. So, stay updated to remain compliant.

- Professional Skepticism and Ethics: Ultimately, maintain high ethical standards. If a client overtly requests you to certify something improper (say, a false purpose of remittance or an artificially split payment to avoid thresholds), refuse the engagement. No fee can justify risking your license and freedom. The PMLA case outcome supports honest CAs, but it will not shield intentional wrongdoing. Following the ICAI Code of Ethics and pronouncements is the best safeguard: do not aid or abet any transaction that you suspect to be unlawful. When in doubt, consult peers or legal counsel rather than rubber-stamp a questionable deal.

By adhering to these best practices, CAs can confidently perform their role in issuing Form 15CB certificates, ensuring both compliance with tax laws and protection from legal risks. The Supreme Court’s judgment serves as a reminder that if CAs “discharge their duties following the professional behavior expected”, the law will shield them against unwarranted criminal prosecution.

Conclusion

The Supreme Court’s Form 15CB judgment is a landmark for financial and compliance professionals in India. It underscores that regulatory compliance actions by a CA, done in good faith, do not equate to criminal conduct under PMLA. This delineation strengthens the hands of honest professionals while ensuring that anti-money laundering efforts remain focused on actual perpetrators. Going forward, Chartered Accountants can perform their certification functions with greater peace of mind, even as they remain vigilant. The case of Murali Krishna Chakrala highlights the fine line between facilitation and complicity – and the courts have drawn it in the right place. In the broader landscape of money laundering compliance in India, this judgment strikes a healthy balance: it enforces accountability where due, but also affirms that compliance professionals are partners – not targets – in the fight against financial crime.

By internalizing the lessons from this case and following best practices, CAs can mitigate their risks and uphold the trust placed in them. The legal precedent set by the Madras High Court (now confirmed by the Supreme Court) will guide future disputes, ensuring that “professional duty ≠ criminal conspiracy” remains the governing mantra. Ultimately, a well-informed and ethical CA community is the best defense against both tax evasion and money laundering – and this ruling empowers just that vision of Chartered Accountant risk management and responsibility in India’s financial system.

Supreme Court Clarifies CA Liability: Issuing Form 15CB Not Equating to Money-Laundering Abetment

Case Title: The Deputy Director v. Murali Krishna Chakrala — SLP (Criminal) Diary No. 8123/2024

Background & Key Legal Framework – Recently, the K. Murali Krishna Chakrala case (see: Murali Krishna Chakrala v. Deputy Director, Directorate of Enforcement – [2023] 457 ITR 579 (Madras HC) and SLP (Crl) Diary No. 8123/2024 in the Supreme Court of India) has become an essential reference point for practising Chartered Accountants in India.

Related Case: Murali Krishna Chakrala v. The Deputy Director, Directorate of Enforcement, Chennai — [2023] 457 ITR 579 (Madras HC)

income tax notice solution, income tax notice u/s 142(1), faceless assessment reply, ITR-U filing, SFT high value transaction notice, CA for income tax notice, income tax notice consultant Dwarka

Leave a Reply