Bitcoin & other Cryptocurrencies will be the cause of the next Financial Crisis – Shaktikanta Das, RBI Governor Posted by By CA ALOK KUMAR December 24, 2022Posted inBitCoin, CBDC, CryptoCurrency, Digital Currency, Future Currency, RBI, RBI GovernorNo Comments Bitcoin and other cryptocurrencies will be the cause of the next financial crisis: Shaktikanta Das, Governor of the RBI

NRI Taxation – Non-Resident Taxpayers can file Form 10F Manually till March 31, 2023 to Claim TDS Benefit Posted by By CA ALOK KUMAR December 23, 2022Posted inForm 10F, Income Tax Act 1961, NRI Taxation, Tax Residency Certificate, TRCNo Comments NRI Taxation - Non-Resident Taxpayers can file Form 10F manually until March 31, 2022 to Claim TDS Benefit

Expenditure During the Establishment & Commencement of a New Business are Deductible: ITAT Pune Bench Posted by By CA ALOK KUMAR December 23, 2022Posted inCourt Judgement, Direct Tax, Income Tax, Income Tax Act 1961No Comments Expenditure During the Establishment & Commencement of a New Business are Deductible: ITAT Pune Bench

Important measures to safeguard yourself from credit card fraud Posted by By CA ALOK KUMAR December 17, 2022Posted inIncome Tax Act 1961No Comments Important measures to safeguard yourself from credit card fraud

In light of the Supreme Court’s EWS ruling, a petition seeks Tax Exemption for Low-Income Families – The Madras HC issued Notice to the Union Government Posted by By CA ALOK KUMAR December 16, 2022Posted inCentral Government, Court Judgement, EWSNo Comments In light of the Supreme Court's EWS ruling, a petition seeks Tax Exemption for Low-Income Families - The Madras HC issued Notice to the Union Government

CSR – Government has modified the Regulations Governing Corporate Social Responsibility Posted by By CA ALOK KUMAR December 15, 2022Posted inCorporate Laws, Corporate Social Responsibility, CSR, Income Tax Act 1961No Comments CSR - Government has modified the Regulations Governing Corporate Social Responsibility

Jewellery held by Minor Son and Daughter: Benefit of CBDT Circular can be Extended Posted by By CA ALOK KUMAR December 14, 2022Posted inDirect Tax, High Court, Income Tax, Income Tax Act 1961, Judicial Decision, source of incomeNo Comments Benefit of CBDT instruction no 1916 providing Ceiling on Holding of Jewellery can be Extended to Jewellery held by Minor Son and Daughter: ITAT

Reassessment of Custom Duty based on Revision Notification is Invalid -Gujarat HC Grants Duty Refund to Adani Wilmar Ltd. Posted by By CA ALOK KUMAR December 14, 2022Posted inAdani Wilmar, Court Judgement, Custom Duty, High Court, Judicial DecisionNo Comments Reassessment of Custom Duty based on Revision Notification is Invalid -Gujarat HC Grants Duty Refund to Adani Wilmar Ltd.

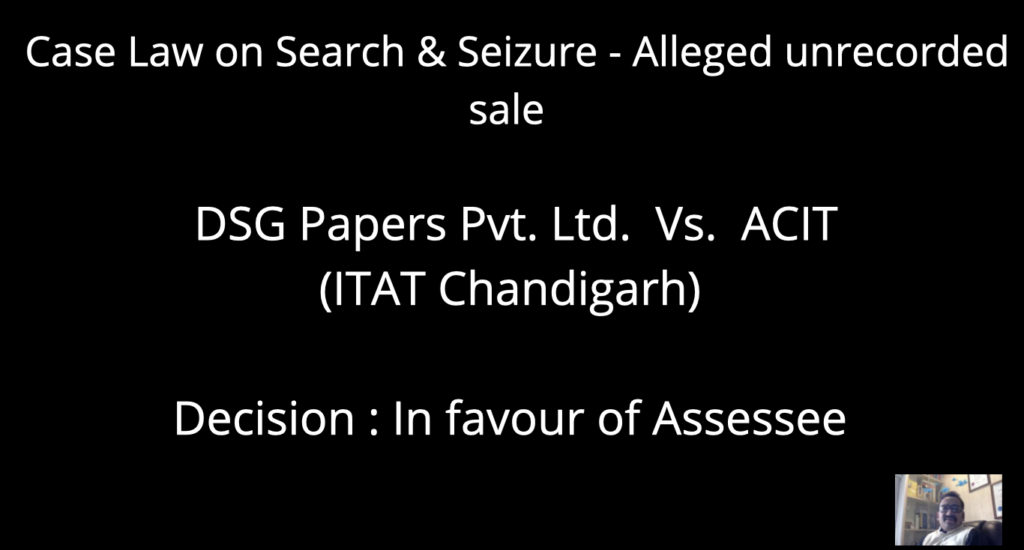

Search & Seizure – Alleged unrecorded sale Posted by By CA ALOK KUMAR December 14, 2022Posted inDirect Tax, Income Tax, Income Tax Act 1961No Comments Search & Seizure - Alleged unrecorded sale

Income Tax Slab Rate Under New Tax System & Old Tax Regime – Its Important for TaxPlanning Posted by By CA ALOK KUMAR December 14, 2022Posted inCentral Government, Direct Tax, Finance Acts, Income Tax, Income Tax Act 1961, source of incomeNo Comments Income Tax Slab Rate Under New Tax System & Old Tax Regime - Its Important for TaxPlanning

![In light of the Supreme Court's EWS ruling, a petition seeks tax exemption for low-income families. The Madras HC issued Notice to the Union Government. Given the recent Supreme Court (SC) decision upholding the validity of the 103rd Constitutional Amendment providing reservation to economically weaker sections (EWS) of society with gross annual income below Rs7,99,999, the Madurai Bench of the Madras High Court (HC) has requested the response of the Centre on a petition (Case No: WP(MD) 26168 of 2022) challenging the fixation of Rs2,50,000 as the base income for the purpose of collecting income-tax. On Monday, the justice R Mahadevan and justice Sathya Narayana Prasad bench adjourned the case for four weeks and directed notice to the union ministries of law and justice, finance, personnel, and public grievance. Agriculturist and asset protection council member Kunnur Seenivasan, the petitioner, asked the court to invalidate the First Schedule, Part-I, paragraph-A of the Finance Act of 2022, which sets the rate of I-T. According to the Schedule, anyone whose combined income is less than Rs. 2,50,000 is free from paying tax. The petitioner contested this Schedule in light of the recent Supreme Court ruling in Janhit Abiyan v. Union of India, which upheld the 10% reservation for the economically backward community while also confirming that a family from a socially forward community with income up to the limit of Rs. 7,99,999 per year, excluding assets, is an EWS family. In his petition, the petitioner made clear that if the government decided to classify a certain group or section of people as EWS in order to receive reservations by establishing gross income, the same standard should be applied to all other groups of people and it shall not collect I-T from all EWS individuals. Therefore, it is necessary to declare the First Schedule, Part-I, paragraph-A of the Finance Act, 2022, [No. 6 of 2022], as ultra-vires and in violation of Articles 14, 15, 16, 21 and 265 of the Indian Constitution. In his suit, Mr. Seenivasan also stated that the objectives of other provisions found in Articles 15 and 16 of the Indian Constitution were defeated by the office memorandum issued by the Centre setting Rs 8,00,000 per year as the condition for economic reservation. The current I-T Act schedule is against the SC ruling since it would result in taxing the economically underprivileged citizens, who would then be unable to compete with those from the forward community in terms of status, education, or economics. Honourable Supreme Court maintains the constitutionality of the EWS quota in a majority decision. The Supreme Court ruled that the 10% EWS quota for the "poorest of the poor" among advanced castes posed no threat to the Constitution's Basic Structure. The 103rd Constitutional Amendment, which grants 10% reservation in government jobs and educational institutions to the "economically weaker sections of the society," was upheld by the Supreme Court's Constitution Bench in a 3:2 majority decision. However, it does not apply to the "poorest of the poor" among Scheduled Castes (SC), Scheduled Tribes (ST), Socially and Educationally Backward Classes (SEBC), and Other Backward Classes (OBC). The majority opinions on the five-judge bench were presented by Justices Dinesh Maheshwari, Bela M. Trivedi, and J.B. Pardiwala during an hour-long session that marked the first time a Constitution Bench decision was live aired. On his final day of employment, Chief Justice U.U. Lalit and Justice S. Ravindra Bhat presented the minority opinion that Justice Bhat had written. Justice Maheshwari took the broad view that reservation was a "instrument of affirmative action by the state" and should not be limited to just SCs, STs, SEBCs, and the non-creamy layer of OBCs, but also include "any class or sections so disadvantaged as to answer the description of "weaker section"" when addressing whether reservation on the sole basis of economic criteria violated the Basic Structure of the Constitution. The legislature "understands and recognises the demands of its own people," Justice Trivedi said. The three judges who made up the majority ruled that the Constitution's Basic Structure was not violated by reservations based solely on economic considerations. Justice Bhat and Chief Justice Lalit, who were in the minority, stated that while quota based on economic deprivation, destitution, and poverty were "per se permissible/valid" and even "constitutionally indefeasible," "othering" of socially and educationally disadvantaged classes, such as the SC/ST/OBC/SEBC communities on the grounds that they already benefit from a pre-existing 50% reservation on the basis of their caste and class origins The majority of the economically disadvantaged sector of society, according to government figures, belonged to SC/ST/SEBC/OBC, hence such an exclusion was simply "Orwellian," according to him. He said that of the country's 31.7 crore people living below the poverty line, the SCs make up 38% of the population, the STs 48.4%, and the OBCs 13.86%. Only 5.85% of people who live below the poverty line (BPL) belong to the forward castes or unreserved group. The petitioners had stated that only the "middle class" of the advanced castes who earned less than 8 lakh as a household annually were left to benefit from the EWS quota due to the exclusion of SC/ST/SEBC/OBC. It is impossible to describe the Amendment as a stunning, cynical perversion of equal justice. Equals cannot be handled unequally, and vice versa for inequalities. Treating unequals fairly will violate Article 14's equality clause, according to Justice Trivedi. The claim that the 10% EWS quota will exceed the 50% reservation cap was rejected by Justice Maheshwari. He said that the Supreme Court's 50% rule, established in the 1992 Indira Sawhney decision, was "not rigid." Furthermore, it had not been applied to the general category but just to the SC/ST/SEBC/OBC communities. But Justices Maheshwari and Bhat concurred that the state had the authority to enact unique rules for implementing reservation in for-profit schools, including professional colleges. The Amendment "cannot be considered to contravene Basic Structure by allowing the state to adopt special rules in connection to admission to private unaided institutions," according to Justice Maheshwari. Reservation cannot "per se be in violation of the Basic Structure" in institutions where education is provided, according to Justice Bhat. He said that if not for the exclusion of the other backward classes, the Amendment would be lawful.](https://caalokkumar.com/my-writing/wp-content/uploads/2022/12/Screenshot-2022-12-16-at-7.25.11-PM.png)