The Income Tax Appellate Tribunal (ITATDelhi )’s bench ruled that the assessee’s residential status should be Determined after taking their passport into account. The assessee filed an appeal against the Commissioner of Income Tax of Delhi’s decision on the assessee’s residency.

The assessing officer had held it against the assessee on the grounds that his stay for more than 180 days overseas was not supported by any proof, including his passport. The dispute centred on the issue of the assessee’s nonresident status for the pertinent assessment year 2017–18. M. P. Rastogi, the assessee’s attorney, claimed that although the copy of the assessee’s passport was filed during the appellate processes, the commissioner of Income Tax (CIT (A)) did not take it into consideration. Sanjay Kumar, the revenue’s attorney, was unable to contest this fact.

The Coram, which was made up of the judicial member Anubhav sharma and the accountant member Shamim yahya, concluded that “no remark was made for not accepting the passport as evidence and which does not require much verification. When the commissioner of income tax (CIT (A)) made a mistake, the assessee’s appeal was granted for statistical reasons. The issue of taking into account passport entry evidence when determining the assessee’s residency status has been returned to the files of the commissioner of income tax (CIT (A)).

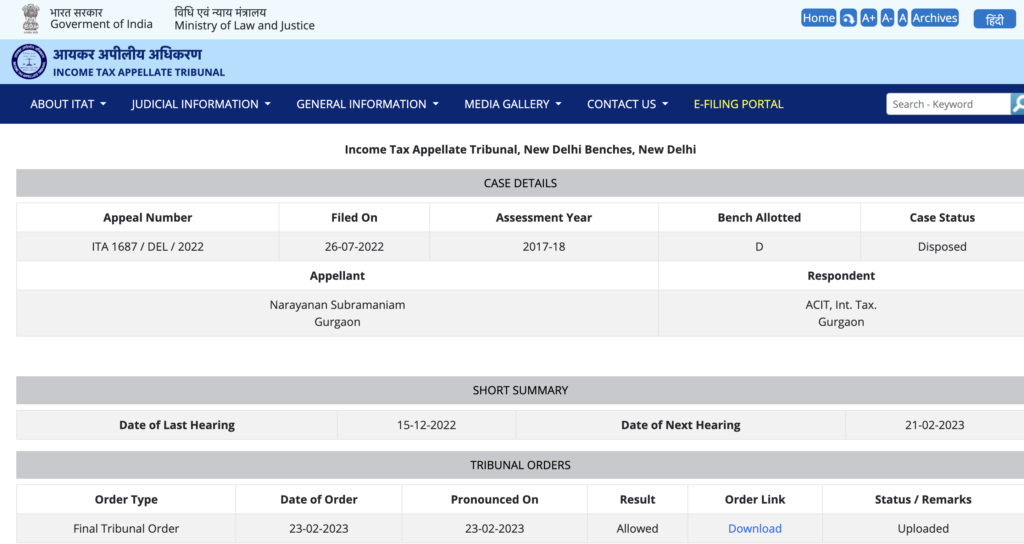

Narayanan Subramaniam Vs ACIT, International Taxation,

Case Number: ITA No. 1687/Del/2022

Date of Judgement: 23/02/2023

INCOME TAX APPELLATE TRIBUNAL DELHI BENCH

BEFORE SHRI SHAMIM YAHYA, ACCOUNTANT MEMBER AND

SHRI ANUBHAV SHARMA, JUDICIAL MEMBER

ITA No. 1687/Del/2022 (Assessment Year: 2017-18)

1309A Beverly Park 2, MG Road, DLF Phase 2, Gurgaon, Haryana-122002

Vs. ACIT, International Taxation, Gurgaon (Appellant) (Respondent)

PAN: AAVPS5624B

Assessee by : Sh. M. P. Rastogi, CA

Revenue by: Sh. Sanjay Kumar, Sr. DR

Date of Hearing 21/02/2023

Date of pronouncement 23/02/2023

PER ANUBHAV SHARMA, J. M.:

1. The appeal has been preferred by the assessee against the order dated 30.05.2022 of Ld. Commissioner of Income Tax (Appeals)-43, Delhi (hereinafter referred as Ld. First Appellate Authority or in short Ld. ‘FAA’) in appeal No. 10321/2019-20 for Assessment Year 2017-18 arising out of an appeal before it against the order dated 22.12.2019 passed u/s 143(3) of the Income Tax Act, 1961 (hereinafter referred as ‘the Act’) by the ld AO,ACIT, International Taxation, Gurgoan (hereinafter referred as the Ld. AO).

2. Heard and perused the record.

3. At the outset it was mentioned on behalf of the assessee by the ld AR that the vital piece of documents being the copy of passport was filed during the appellate proceedings but it was not considered by the ld CIT(A) and no finding was given and for which ground no 1 is raised. The ld DR could not dispute this fact.

ITA No. 1687/Del/2022 Narayanan Subramaniam

4. Appreciating the matter on record it comes up that the controversy involved is primarily with regard to question if the assessee had nonresidential status for the relevant Assessment Year 2017-18 and the ld AO had held it against the assessee on the basis that his stay for more than 180 days abroad was not supported by any evidence including passport. The ld CIT(A)’s order shows that at the appellate stage the assessee had filed submissions dated 18.08.2020 which are available at page No. 4 to 39 of the paper book which has been reproduced at page Nos. 3 to 5 of the ld CIT(A)’s order and therein it was specifically mentioned “the details of number of days in India in FY 2016-17 again being enclosed herewith along with copy of passport of the appellant.” Inspite of it the ld CIT(A) considered it to be a case where the residential status of the appellant could not be ascertained in absence of passport.

No observation was made for not considering the passport as evidence and which does not require much verification. The ld CIT(A) had fallen in error and thus, ground No. 1 as raised in the appeal deserved to be sustained. 5. The appeal of the assessee is allowed for statistical purposes. The issue of consideration of the evidence in the form of passport entry for determination of the residential status of the assessee is restored to the files of the ld CIT(A).

Order pronounced in the open court on 23/02/2023.

Sd/- -Sd/-

(SHAMIM YAHYA). (ANUBHAV SHARMA)

ACCOUNTANT MEMBER JUDICIAL MEMBER

Dated: 23/02/2023

A K Keot Copy forwarded to

1. Applicant

2. Respondent

3. CIT

4. CIT (A)

5. DR:ITAT ASSISTANT REGISTRAR ITAT, New Delhi

Leave a Reply