Dear Reader

I am here to help you with your taxes on income. My objective is to provide you with the necessary guidelines for the proper accounting treatment of taxes on income.

AS 22 stands for Accounting Standard 22. It is a set of guidelines issued by the Institute of Chartered Accountants of India (ICAI) that prescribes the accounting treatment for taxes on income.

What is the prime objective of AS 22 – Taxes on Income

The objective of AS 22 is to prescribe the accounting treatment for taxes on income. Taxes on income are one of the significant items in the statement of profit and loss of an enterprise. In accordance with the matching concept, taxes on income are accrued in the same period as the revenue and expenses to which they relate.

The scope of AS 22 is to be applied in accounting for taxes on income. It covers the recognition, measurement, presentation, and disclosure of taxes on income. The standard applies to all enterprises, regardless of their size or nature of business, and it covers all types of taxes on income, including those levied by foreign governments.

What is Deferred Tax as per As22

AS 22 defines deferred tax as the tax effect of timing differences. Timing differences are the differences between taxable income and accounting income that arise because certain items of revenue or expense are recognized in one period for tax purposes and another period for accounting purposes. Deferred tax assets and liabilities arise from timing differences, and they represent the future tax consequences of those differences. The standard provides guidelines for recognizing, measuring, presenting, and disclosing deferred tax assets and liabilities.

What is Timing difference as per AS22

AS 22 defines timing differences as the differences between taxable income and accounting income for a period that originate in one period and are capable of reversal in one or more subsequent periods. Timing differences arise because the period in which some items of revenue and expenses are included in taxable income do not coincide with the period in which such items of revenue and expenses are included or considered in arriving at accounting income. For example, machinery purchased for scientific research related to business is fully allowed as a deduction in the first year for tax purposes whereas the same would be charged to the statement of profit and loss as depreciation over its useful life.

What is Permanent Difference as per AS22

- AS 22 defines permanent differences as the differences between taxable income and accounting income that will never reverse in the future. Permanent differences arise because some items of revenue or expense are included in taxable income but are not considered in arriving at accounting income, or vice versa. For example, dividend income received from a subsidiary is exempt from tax under the Income Tax Act but is included in accounting income. Similarly, expenses incurred on entertainment are not allowed as a deduction for tax purposes but may be charged to the statement of profit and loss as an expense. Permanent differences do not give rise to deferred tax assets or liabilities because they do not affect future tax payments.

What is the difference between Current Tax and Deferred Tax as per AS22

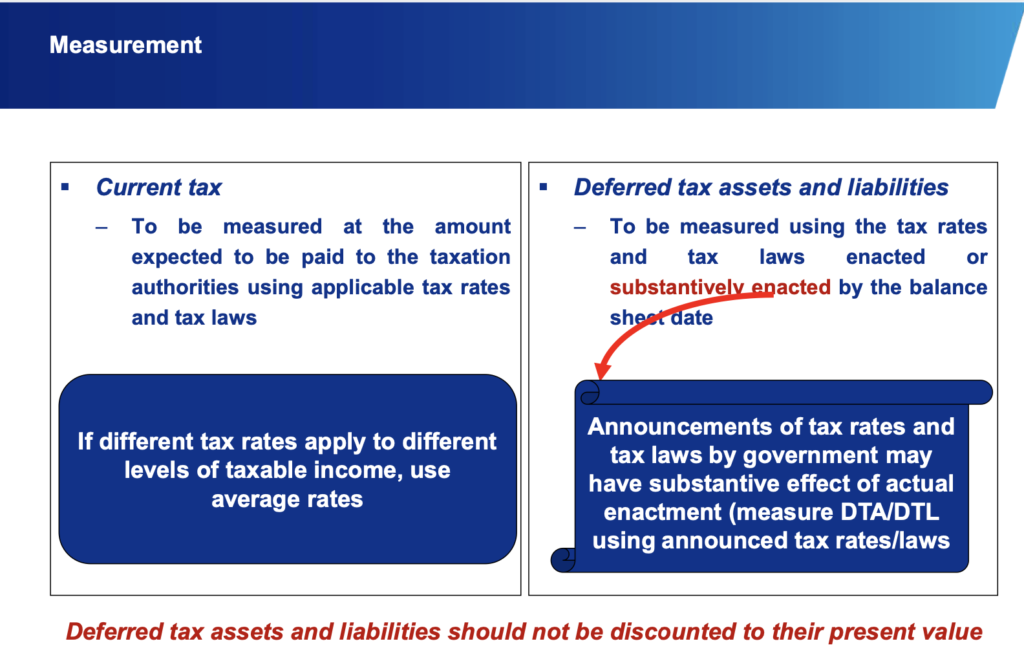

AS 22 defines current tax as the amount of income tax payable or recoverable in respect of the taxable income for a period. It is based on the taxable income computed using the tax laws and rates that have been enacted or substantively enacted at the end of the reporting period. Current tax is recognized as an expense or income in the statement of profit and loss for the period.

Deferred tax, on the other hand, is the tax effect of timing differences. Timing differences are differences between taxable income and accounting income that originate in one period and are capable of reversal in one or more subsequent periods. Deferred tax assets and liabilities arise from timing differences, and they represent future tax consequences of those differences. Deferred tax assets and liabilities are measured using enacted or substantively enacted tax rates and laws that will apply to taxable income in future periods when those timing differences reverse.

In summary, current tax is based on taxable income for a period using current tax laws and rates, while deferred tax arises from timing differences between taxable income and accounting income that will reverse in future periods using future enacted or substantively enacted tax laws and rates.

What is the Recognition process for Deferred Tax Assets as per AS 22

An enterprise recognizes deferred tax assets only to the extent that it has timing differences, the reversal of which will result in sufficient income or there is other convincing evidence that sufficient taxable income will be available against which such deferred tax assets can be realized. In such circumstances, the nature of the evidence supporting its recognition is disclosed.

In other words, an enterprise recognizes a deferred tax asset when it is probable that there will be future taxable profits against which the asset can be utilized. The recognition of a deferred tax asset is based on management’s estimate of future taxable profits and is subject to review by auditors.

If an enterprise has a history of losses or if there are no convincing indications that sufficient taxable profits will be available in future periods, then no deferred tax asset should be recognized. However, if an enterprise subsequently realizes that it has sufficient taxable profits against which a previously unrecognized deferred tax asset can be utilized, then the asset should be recognized in the period in which it becomes probable that sufficient taxable profits will be available.

In summary, an enterprise recognizes a deferred tax asset only when it is probable that there will be future taxable profits against which the asset can be utilized. The recognition process involves estimating future taxable profits and subjecting them to review by auditors.

What is the Presentation and Disclosure Requirements for Taxes on Income under AS22?

AS 22 prescribes the following presentation and disclosure requirements for taxes on income:

1. Presentation of current tax: The amount of current tax should be presented as a separate item in the statement of profit and loss.

2. Presentation of deferred tax: Deferred tax assets and liabilities should be presented as separate line items in the balance sheet.

3. Disclosure of deferred tax: The nature of the timing differences that give rise to deferred tax assets and liabilities should be disclosed, along with the amount of each type of asset or liability.

4. Reconciliation of deferred tax: A reconciliation between the opening and closing balances of deferred tax assets and liabilities should be provided, showing separately the changes arising from acquisitions, disposals, revaluations, and other movements.

5. Disclosure of unrecognized deferred tax assets: The amount of any unrecognized deferred tax assets should be disclosed, along with an explanation for why they have not been recognized.

6. Disclosure of unrecognized deferred tax liabilities: The amount of any unrecognized deferred tax liabilities should be disclosed, along with an explanation for why they have not been recognized.

7. Disclosure of current and deferred taxes related to items charged or credited directly to equity: Any current or deferred taxes related to items charged or credited directly to equity (such as revaluation reserves) should be disclosed separately.

In summary, AS 22 requires separate presentation and disclosure for current taxes, deferred taxes, and unrecognized deferred taxes in the financial statements. It also requires a reconciliation between opening and closing balances for deferred taxes along with disclosure requirements for various types of movements in these balances.

Reassessment of Unrecognized Deferred Tax Assets under AS22

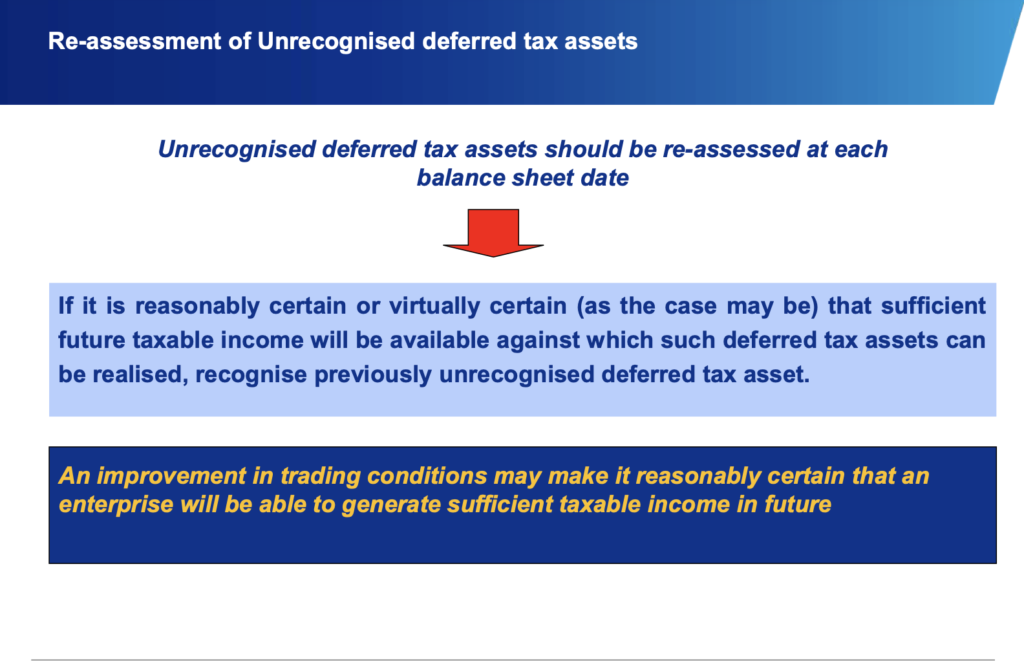

AS 22 requires an enterprise to re-assess unrecognised deferred tax assets at each balance sheet date. The enterprise should recognise previously unrecognised deferred tax assets to the extent that it has become reasonably certain or virtually certain, as the case may be, that sufficient future taxable income will be available against which such deferred tax assets can be realised. For example, an improvement in trading conditions may make it reasonably certain that the enterprise will be able to generate sufficient taxable income in the future.

The re-assessment of unrecognised deferred tax assets is important because it ensures that an enterprise does not overstate its assets by recognising deferred tax assets that are unlikely to be realised in the future. By re-assessing these assets at each balance sheet date, an enterprise can ensure that its financial statements provide a true and fair view of its financial position.

- In summary, AS 22 requires an enterprise to re-assess unrecognised deferred tax assets at each balance sheet date and recognise them only if it is reasonably certain or virtually certain that sufficient future taxable income will be available against which such deferred tax assets can be realised. This helps ensure that an enterprise’s financial statements provide a true and fair view of its financial position.

Examples of Timing Difference under AS22

AS 22 defines timing differences as differences between taxable income and accounting income that originate in one period and are capable of reversal in one or more subsequent periods. Some examples of timing differences are:

1. Depreciation: The depreciation charged in the statement of profit and loss may be different from the depreciation allowed for tax purposes. This creates a timing difference that will reverse when the asset is sold or disposed of.

2. Accruals and provisions: Accruals and provisions made in the statement of profit and loss may not be deductible for tax purposes until a later period, creating a timing difference.

3. Revenue recognition: Revenue recognized in the statement of profit and loss may be different from revenue recognized for tax purposes due to different recognition criteria, creating a timing difference.

4. Capital gains: Capital gains may be taxed at a different rate than ordinary income, creating a timing difference.

5. Tax losses carried forward: Tax losses carried forward from previous periods may be used to offset future taxable profits, creating a timing difference.

In summary, timing differences arise due to differences between taxable income and accounting income that originate in one period and are capable of reversal in one or more subsequent periods. Examples include depreciation, accruals and provisions, revenue recognition, capital gains, and tax losses carried forward.

AS 22 provides several illustrations to help explain the concepts and requirements of the standard. These illustrations are intended to be examples only and should not be considered exhaustive or definitive.

One example of an illustration provided in AS 22 is as follows:

Illustration 1: Recognition of Deferred Tax Assets

An enterprise has a timing difference of Rs. 100,000 at the end of the current year, which will result in a deductible amount of Rs. 120,000 in the future when the timing difference reverses. The enterprise has no other timing differences.

The enterprise estimates that it will have taxable profits of Rs. 150,000 in each of the next two years against which the deferred tax asset can be utilized.

In this case, the enterprise recognizes a deferred tax asset of Rs. 30,000 (Rs. 120,000 x 25%) because it is probable that there will be sufficient taxable profits against which the asset can be utilized.

This illustration demonstrates how an enterprise recognizes a deferred tax asset when it is probable that there will be future taxable profits against which the asset can be utilized.

- In summary, AS 22 provides several illustrations to help explain its concepts and requirements. These illustrations are intended to be examples only and should not be considered exhaustive or definitive. One such illustration demonstrates how an enterprise recognizes a deferred tax asset when it is probable that there will be future taxable profits against which the asset can be utilized.

Leave a Reply