Biryani Bills to Big Data: How AI Helped Income Tax Detect ₹408 Crore Hidden Restaurant Turnover

Income Tax Department’s Restaurant Turnover Verification Drive: A Wake-Up Call for India’s Food & Beverage Sector

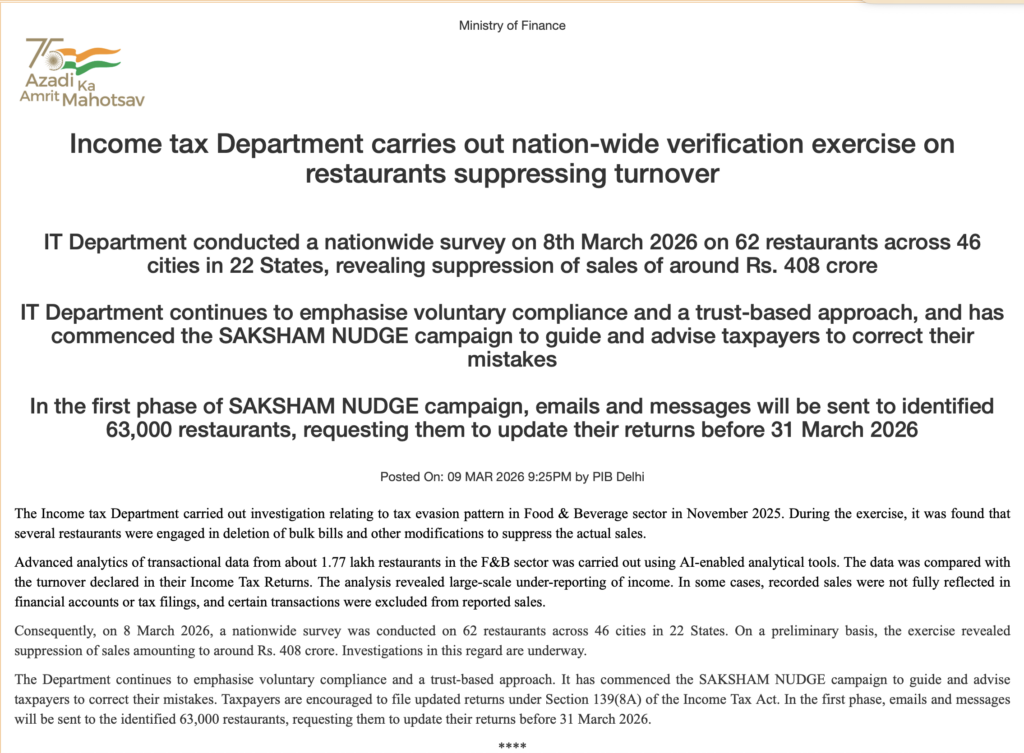

The Income Tax Department’s latest verification exercise in the restaurant industry is not just another tax news item. It is a strong signal that data analytics, AI tools, transactional trails, and return disclosures are now being read together. In its 9 March 2026 press release, the Government stated that the Department analysed transactional data from about 1.77 lakh restaurants, compared it with figures reported in income-tax returns, and found patterns suggesting deletion of bills and other modifications aimed at suppressing actual sales.

The official release further states that, on 8 March 2026, a nationwide survey was conducted on 62 restaurants across 46 cities in 22 States, and the preliminary outcome indicated suppression of sales of around ₹408 crore. The Department also said that investigations are underway. In parallel, it has launched the SAKSHAM NUDGE campaign, under which emails and messages are to be sent to around 63,000 identified restaurants, asking them to update their returns before 31 March 2026.

For restaurant owners, accountants, tax consultants, and software-driven businesses, this development matters far beyond the food sector. It demonstrates that the tax administration is increasingly relying on technology-led verification rather than only traditional scrutiny. It also shows that where digital records, billing systems, and tax filings do not align, the risk of detection is much higher than before.

What exactly did the CBDT say?

According to the PIB release issued by the Ministry of Finance, the Income Tax Department had started investigating tax evasion patterns in the Food & Beverage sector in November 2025. During this process, it found that some restaurants were allegedly engaged in deletion of bulk bills and other data changes to understate actual turnover. The Department then used AI-enabled analytical tools to compare transactional data with income disclosed in income-tax returns and identified large-scale under-reporting.

This is significant because the official narrative is not merely about “raids” or “surveys”; it is about a technology-backed mismatch analysis. In simple words, if the back-end data, POS records, settlement reports, ledgers, and return disclosures tell different stories, the mismatch itself becomes the trigger. That is the larger message coming out of this action.

Why this matters so much for restaurants

Restaurants are cash-intensive, high-volume, and operationally fast-moving businesses. Billing errors, manual overrides, discount misuse, complimentary entries, deleted KOTs, aggregator reconciliation gaps, or POS-to-books mismatches can arise either through weak systems or deliberate manipulation. In such a sector, even small control failures repeated over thousands of transactions can create major exposure. The Department’s use of large-scale analytics suggests that these patterns are now being studied in bulk, not case by case.

Media reporting on the exercise indicates that investigators looked at software trails, accounting records, and digital evidence such as server logs and POS data. While the official PIB release focuses on the broad findings, these reports indicate the practical direction of inquiry: Was turnover fully captured? Was reported revenue consistent with transactional evidence? Were records modified after the event?

The rise of AI-driven tax enforcement

One of the most important takeaways from this episode is the increasing use of AI-enabled analytics in tax administration. The PIB release expressly mentions that the Department analysed large transactional datasets using AI-enabled tools. That means compliance risk is no longer limited to notices triggered by obvious return mismatches; it now extends to hidden behavioural patterns across software systems, transaction frequencies, unusual deletions, and inconsistencies between reported income and operational data.

For businesses, this changes the compliance mindset. Earlier, many taxpayers treated books of account, billing software, GST data, and income-tax disclosures as parallel silos. That approach is increasingly unsafe. A modern compliance framework requires one clean financial narrative across all systems. If the sales shown in internal software, books, GST filings, TDS records, bank receipts, and income-tax returns are not reconcilable, the problem is no longer merely clerical; it can become evidentiaryIs this only about restaurants?

Today’s action is sector-specific, but the principle is much broader. If such analytics can be applied to restaurants, the same model can be extended to other sectors where there is high transaction velocity, fragmented data, platform dependence, and scope for manual overrides. Retail, healthcare, distribution, e-commerce-linked sellers, salons, hospitality, and service businesses should all treat this development as a compliance warning. This is an inference from the Department’s analytical approach and not a separate official announcement.

What is the relevance of Section 139(8A) and updated returns?

The official press release states that the Department is encouraging identified restaurants to update their returns under Section 139(8A) before 31 March 2026. The e-filing portal also confirms that utilities for filing updated returns are available.

This is important because the Department is coupling enforcement with a voluntary compliance opportunity. The message is clear: where a taxpayer has made an omission, the system is giving a limited window to correct it rather than waiting only for coercive proceedings. That policy direction is explicitly reflected in the SAKSHAM NUDGE campaign mentioned in the press release.

What should restaurant owners do immediately?

The first step is not panic; it is forensic reconciliation. Businesses should review whether the turnover recorded in the POS, food delivery platform reports, bank settlements, cash registers, management MIS, and final books of account actually matches the turnover declared in income-tax and GST filings. Any difference should be identified, explained, and documented quickly. That is the most practical response to a data-driven verification environment. The need for this step follows directly from the mismatch-based findings described in the official release.

The second step is to examine system controls. Management should ask: Who can delete bills? Who can edit a day’s sales after closure? Are audit trails enabled? Are deleted or voided transactions independently reviewed? Is there any dual-database structure, back-end modification route, or local override risk? Media reports around this action suggest that software-level tampering and digital record trails are under focus.

The third step is legal and tax evaluation. If omissions are real, the business should obtain a professional review on whether and how an updated return may be filed, what tax cost may arise, and what disclosures should be made consistently across direct tax, GST, books, and audit documentation. The official portal confirms that updated return utilities are available, but the exact strategy must depend on the relevant assessment year, facts, and applicable law.

Practical compliance checklist for restaurant businesses

A sensible restaurant compliance review in 2026 should cover these areas:

- POS sales vs books of account reconciliation

- Aggregator sales vs settlement reports vs ledger postings

- Cash sales vs cash deposit trail

- Discount, void, cancellation, and complimentary bill controls

- Stock consumption vs reported sales reasonability

- Day-end closing controls and back-end edit rights

- Branch-wise sales consolidation

- GST turnover vs income-tax turnover comparison

- Vendor purchase trend vs reported sales trend

- Preservation of audit trails, server logs, and accounting backups

This checklist is an original compliance framework based on the risk themes reflected in the Department’s press release and related reporting.

Why professionals should pay close attention

For Chartered Accountants, tax advisors, and internal finance teams, this episode is a reminder that compliance advisory must now move beyond return filing. Clients need systems assurance, reconciliation discipline, and data defensibility. A restaurant may appear compliant on the face of its return, but if the underlying data ecosystem is weak, the risk remains alive. The era of “books are clean because the final ledger is clean” is steadily fading.

This also increases the importance of contemporaneous documentation. If a mismatch is genuine and explainable, the explanation must exist in records, not in memory. Good advisory in this environment means helping clients build a trail that is internally consistent, technologically auditable, and legally defensible. That is the real professional takeaway from the current action. This is an analytical conclusion drawn from the official fact pattern.

A wider policy signal from the government

The broader policy message is balanced but firm. On one hand, the Department is investigating suspected suppression. On the other hand, it is simultaneously promoting a trust-based approach and inviting taxpayers to voluntarily correct mistakes through the SAKSHAM NUDGE campaign. That combination of data intelligence plus voluntary complianceis likely to become the standard model for future tax administration in India.

Businesses should therefore not read this event only as a story about one sector. They should read it as a preview of how compliance oversight may increasingly work across India: identify anomalies digitally, verify them through field action where necessary, and nudge correction before harsher consequences follow. That conclusion is a reasonable inference from the government’s announced approach.

Final word

The restaurant turnover verification exercise is a serious compliance development. The official numbers are substantial: data from 1.77 lakh restaurants analysed, 62 restaurants surveyed across 46 cities in 22 States, and around ₹408 croreof preliminary sales suppression detected, with 63,000 restaurants targeted for compliance nudges. Whether one views this as enforcement, reform, or both, the lesson is the same: digital sales trails must match tax disclosures.

For restaurant businesses, the right response is immediate internal review. For professionals, the right response is deeper advisory. And for all businesses, the message is unmistakable: in the AI era, tax compliance is no longer just about filing a return; it is about whether your entire data story stands together.

FAQ on Restaurant Verification Drive by Income Tax Department in India

1. What did the Income Tax Department find in the restaurant verification drive?

The Department stated that a nationwide exercise revealed preliminary suppression of sales of around ₹408 crore after surveys on 62 restaurants across 46 cities in 22 States.

2. Why were restaurants targeted by the Income Tax Department?

According to the official release, the Department had been investigating tax evasion patterns in the Food & Beverage sector and found indications such as deletion of bulk bills and modifications allegedly used to suppress actual sales.

3. What is the SAKSHAM NUDGE campaign?

It is the Department’s voluntary compliance initiative under which emails and messages are to be sent to identified restaurants, encouraging them to correct mistakes and update returns.

4. How many restaurants may receive such communication?

The first phase of the campaign is to reach around 63,000 restaurants, according to the official press release.

5. What is the deadline mentioned in the press release?

The press release says the identified restaurants are being asked to update their returns before 31 March 2026.

6. Can restaurants file an updated return?

The official communication specifically refers to updating returns under Section 139(8A), and the income-tax portal also shows availability of updated return utilities.

7. What records should restaurant owners review immediately?

They should review POS records, aggregator statements, books of account, cash and bank reconciliations, GST turnover, deleted or voided bills, and any software audit trail or server-level controls. This is a practical compliance recommendation based on the risk themes emerging from the exercise.

When Data Speaks: Income Tax Department Detects ₹408 Crore Suppressed Sales in Restaurant Sector

- ITR filing services

- tax notice / scrutiny assistance

- GST compliance for restaurants and traders

- tax audit and accounting services

- business advisory and internal controls

CA in Dwarka Delhi | Tax Consultant in Delhi | Income Tax Notice Consultant in Delhi | GST Consultant in Delhi | Faceless Assessment Consultant | CA Near Me | ITR Filing in India |

Leave a Reply