India’s Digital Payments Revolution: RBI’s Digital Lending Directions & UPI’s Global Dominance

India’s financial landscape is undergoing a transformation. On 8 December 2025 the Minister of Finance informed the Lok Sabha that the Government and the Reserve Bank of India (RBI) had taken concerted steps to safeguard consumers from rogue digital‑lending platformspib.gov.in. In the same session it was revealed that India’s Unified Payments Interface (UPI) is now the world’s largest real‑time payment system, handling nearly half of all global fast‑payment transactionsndtv.com. This article merges those two developments to show how tighter oversight of digital lending and the meteoric rise of UPI are together propelling India’s digital‑payments revolution.

Strengthening the digital‑lending ecosystem

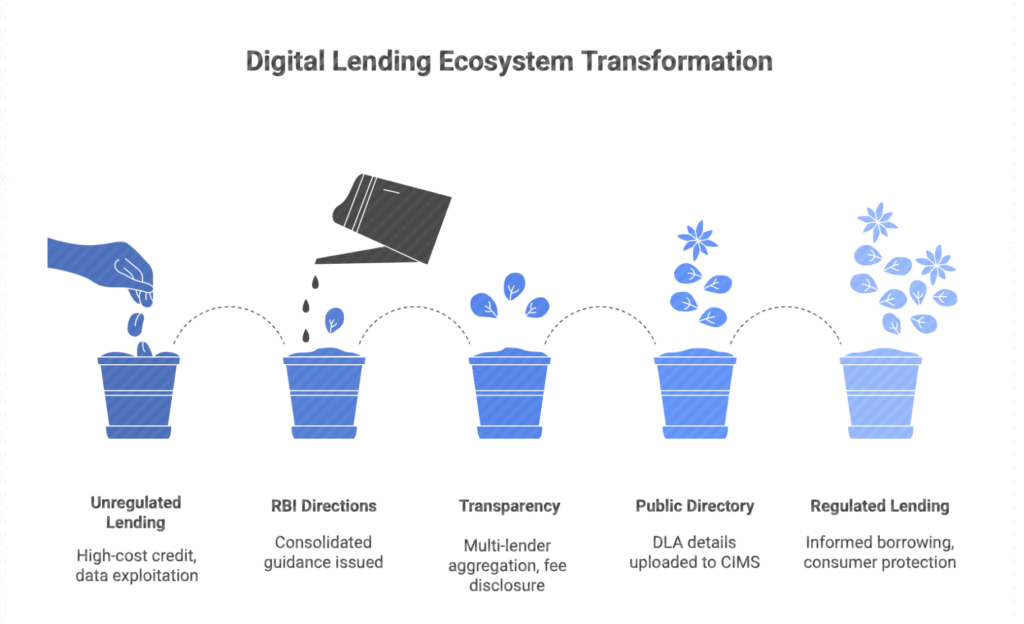

The proliferation of loan apps has exposed consumers to high‑cost credit, data exploitation and aggressive recovery tactics. To combat these abuses, the RBI consolidated its guidance into the Reserve Bank of India (Digital Lending) Directions, 2025, issued on 8 May 2025fidcindia.org.in. Key provisions include:

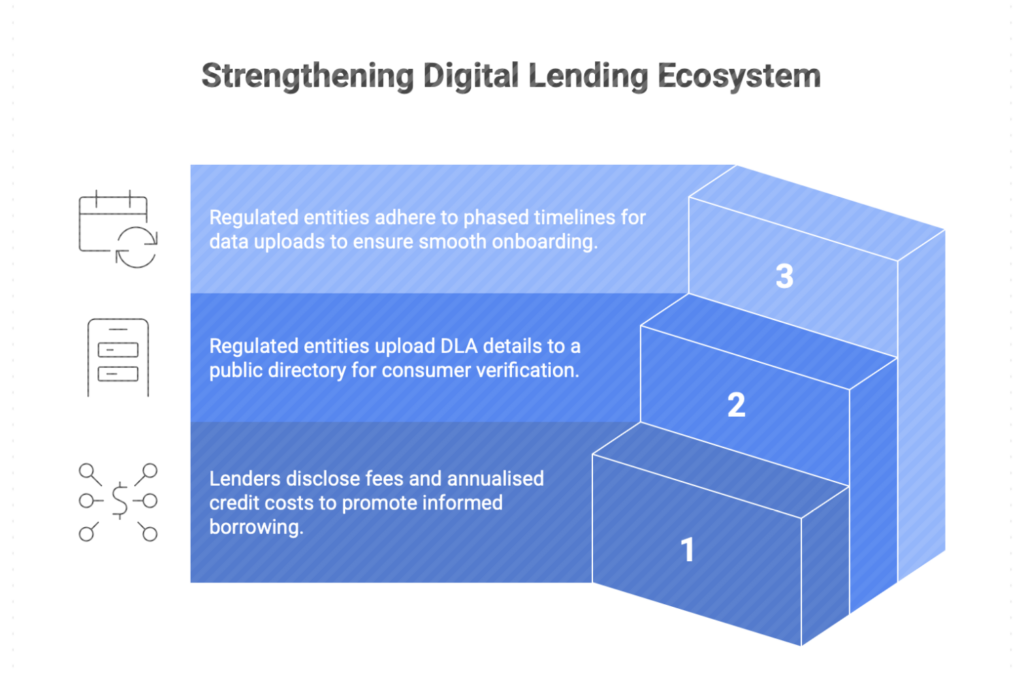

- Transparency and multi‑lender aggregation – Lenders offering a platform where borrowers can compare offers from multiple financiers must disclose all fees and the annualised cost of credit fidcindia.org.in. This promotes informed borrowing and curbs hidden charges.

- Public directory of Digital Lending Apps (DLAs) – Regulated entities must upload details of every DLA they deploy to the RBI’s Centralised Information Management System (CIMS). The directory is updated automatically and is accessible to consumers from 1 July 2025, enabling them to verify whether an app is legitimately linked to a regulated lenderfidcindia.org.in.

- Transition timelines – Regulated entities were required to furnish initial DLA data by 13 May 2025 and complete uploads by 15 June 2025fidcindia.org.in. The phased approach ensured smooth onboarding without disrupting lending services.

These directions were complemented by legal and enforcement measures. The Ministry of Electronics and Information Technology can block unauthorised apps under section 69A of the Information Technology Act 2000 after following the due processpib.gov.in. The Government also engages with internet intermediaries and messaging platforms to clamp down on unregistered loan apps, while the Indian Cyber Crime Coordination Centre (I4C) operates a national portal (cybercrime.gov.in) and helpline (1930) to report fraudpib.gov.in. Complaints relating to illegal deposit‑taking can be lodged through the RBI’s SACHET portal or the inter‑regulatory State Level Coordination Committee(SLCC)pib.gov.in. To improve financial literacy, the RBI conducts e‑BAAT programmes and runs public awareness campaigns on cyber‑crime and data privacypib.gov.in.

Implications for businesses and professionals: Chartered accountants and fintech start‑ups should review the Digital Lending Directions carefully. They mandate clear loan documentation, consent‑based data collection, caps on recovery fees and robust grievance redressal mechanisms. Firms must ensure that any digital lending app they use or recommend is listed in the RBI directory and complies with the privacy and fair‑practice standards. Failure to do so may expose them to regulatory action and reputational risk.

UPI recognised as the world’s largest real‑time payment system

In the same parliamentary reply, the Minister cited the International Monetary Fund’s Fintech Note “Growing Retail Digital Payments – The Value of Interoperability”. The study, released in June 2025, found that UPI is the world’s largest retail fast‑payment system by transaction volumendtv.com. Complementary data from ACI Worldwide’s Prime Time for Real‑Time 2024 report shows that UPI accounts for approximately 49 % of all global real‑time payment transactions, with 129.3 billion transactions processedndtv.com. The scale of UPI dwarfs other systems such as Brazil’s PIX (14 % share), Thailand’s PromptPay (8 %), China’s FPS (6 %) and South Korea’s KFTC HOFInet (3 %)ndtv.com.

| Country / payment system | Transaction volume (billions) | Share of global real‑time payments |

|---|---|---|

| India – UPI | 129.3 | 49 % |

| Brazil – PIX | 37.4 | 14 % |

| Thailand – PromptPay | 20.4 | 8 % |

| China – FPS | 17.2 | 6 % |

| South Korea – HOFInet | 9.1 | 3 % |

| Others | 52.8 | 20 % |

Source: ACI Worldwide, Prime Time for Real‑Time 2024ndtv.com.

Measures to deepen digital payments

The Government, RBI and the National Payments Corporation of India (NPCI) have implemented several schemes to encourage the adoption of UPI and digital payments, particularly among small merchants:

- Incentives for low‑value BHIM‑UPI transactions – Merchants accepting small‑ticket transactions receive subsidies to offset merchant discount rates, reducing the cost of digital acceptance and encouraging cash‑light transactions.

- Payments Infrastructure Development Fund (PIDF) – The PIDF provides grant support to banks and fintechs for deploying point‑of‑sale (POS) terminals and QR codes in tier‑3 to tier‑6 centres. As of 31 October 2025, the fund has facilitated the deployment of approximately 5.45 crore digital touchpoints across smaller towns and rural areas ndtv.com.

- Large‑scale QR code deployment – In FY 2024‑25, roughly 56.86 crore QR codes were deployed to 6.5 crore merchants, greatly expanding the acceptance network ndtv.com.

- RuPay‑UPI integration across sectors – UPI and RuPay are being integrated into public services, transport and e‑commerce platforms nationwide, further embedding digital payments into everyday transactions ndtv.com.

These initiatives have paid off. NPCI data show that UPI processed more than 19 billion transactions worth ₹24.58 lakh crore in November 2025; two years earlier (November 2023) the volume was just 11.16 billion, underscoring the system’s rapid growth tribuneindia.com.

The bigger picture

The dual narratives of stricter lending oversight and explosive digital‑payment adoption reflect India’s broader aim of building a secure, interoperable and inclusive digital‑finance ecosystem. By codifying borrower protections, mandating transparency and establishing a public directory of digital‑lending apps, the RBI is addressing the reputational damage caused by unscrupulous loan platforms. Simultaneously, the success of UPI demonstrates how open, interoperable infrastructure—combined with regulatory support and incentives—can drive massive adoption at low cost.

Professionals advising clients in the financial sector should consider the following action points:

- Due diligence on lending partners – Verify that all digital‑lending partners comply with the Digital Lending Directions 2025 and are listed in the RBI’s DLA directory.

- Compliance with data‑protection norms – Review data‑collection and consent procedures to ensure they align with RBI requirements and emerging personal‑data laws.

- Embrace digital payment infrastructure – Encourage clients to adopt UPI and other real‑time payment channels, leveraging schemes such as PIDF to reduce setup costs.

- Monitor regulatory updates – The digital‑finance landscape is evolving rapidly; staying informed about RBI circulars, notifications and parliamentary discussions will help firms remain compliant and competitive.

Conclusion

India’s digital‑payments journey demonstrates that robust regulation and innovation can coexist. The Digital Lending Directions 2025 tighten the screws on unscrupulous lending, while the phenomenal success of UPI shows how interoperability and incentives can make real‑time payments ubiquitous. As the ecosystem matures, maintaining a balance between consumer protection and innovation will be key to sustaining trust and ensuring that the benefits of digital finance reach every corner of the country.

Leave a Reply